Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

The Latest Fintech: How SNPL Guides the Building of Better Customer Relationships

Fintech, the fusion of finance and technology, has seen increasing momentum in recent years. Amid this trend, a new fintech service called "SNPL," based on the concept of "saving," has emerged.

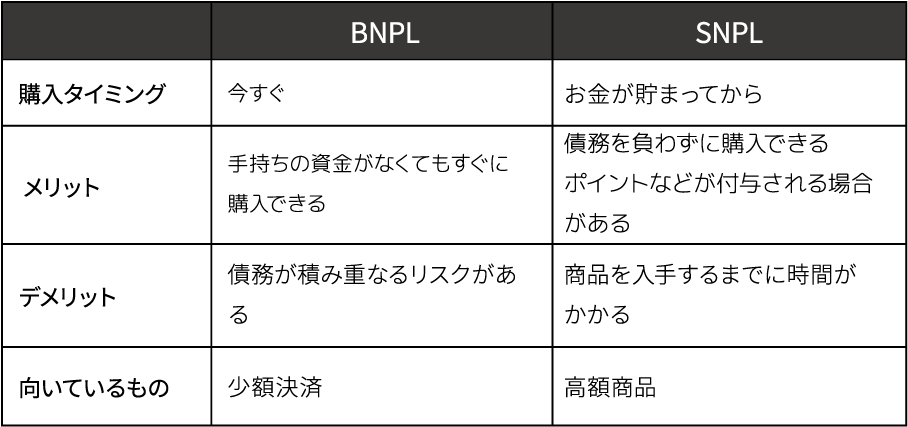

While services like "BNPL (Buy Now, Pay Later)"—where payment is made after purchase—are also expanding, concerns have been raised about their downsides, such as increased costs from unpaid fees or late charges. SNPL is expected to cover these negative aspects of BNPL and foster a healthier, more positive consumption cycle.

This article explores SNPL under the theme "What kind of trust relationship between businesses and consumers does SNPL bring?" Those interested in the latest trends in the fintech market or considering how to build long-term trust with customers should find this a valuable reference.

The Unexpected Pitfalls Hidden in the Popular Convenient Payment Service BNPL

As previously covered in this article, the "BNPL (Buy Now, Pay Later)" payment style is gaining popularity, particularly among Gen Z.BNPL allows consumers to purchase goods upfront and pay later. Its ease of use—requiring no strict credit checks like traditional credit cards—lowers purchase barriers. It has spread widely in Western countries, Australia, and even Southeast Asia, where credit card ownership is low. In Japan, major e-commerce platforms and other companies have launched BNPL services, with further adoption expected.

However, while convenient, BNPL can also be seen as a system that effectively puts consumers into debt. Even when intending to pay later, some users end up missing payment deadlines and unexpectedly accumulating debt. Furthermore, late fees and other charges can apply, and some users may be utilizing the service without fully understanding these costs.

A 2021 survey by Credit Karma, a U.S. company providing credit score information to consumers, revealed that nearly 40% of American consumers who had used BNPL services had missed at least one payment. Of those, 72% experienced a decline in their credit score after the missed payment. This situation has indeed prompted movements in various countries to strengthen oversight of BNPL services.Furthermore, since a "debt" remains outstanding from purchase until payment is completed, users may hesitate to make subsequent purchases the following month or later due to concerns about this outstanding balance.

SNPL is gaining attention as a fintech solution that addresses these drawbacks of BNPL and delivers a new shopping experience.

SNPL: Fintech Enabling a "Save and Pay" Shopping Experience

Let's take a closer look at the features of SNPL and how it differs from BNPL.

SNPL stands for "Save Now, Pay Later," meaning "save before you pay."If BNPL solves the problem of wanting something but lacking funds by "borrowing," SNPL solves it by "saving." For example, when you find something you want on an e-commerce site, using SNPL automatically saves the required amount in an account linked to your bank or credit card. Once the target amount is reached, you can make the purchase. Some services even reward you with points upon reaching your savings goal.

BNPL might be more casual and carry less risk for small payments. On the other hand, for purchasing high-priced items, SNPL, which ensures you save the money before buying, is considered a well-suited service.

One of the leading SNPL services launched in the US in 2021. Immediately after launch, numerous brands, including shoe manufacturers and luxury mattress makers, became partners. Consumers could then select desired items from these partner brands, save the required amount, and make the purchase.

The concept of saving money for something you want is a long-standing, reliable method and not new. However, many people find it difficult to stick to their resolution to "save for an expensive purchase" on their own, or feel that setting up a savings plan at a bank is too much hassle. Many SNPL services, however, build mechanisms that naturally encourage saving.For example, one Japanese SNPL service automates the savings process. After setting a goal and rules, it automatically deducts savings from your credit card, eliminating cumbersome procedures. Furthermore, it boosts motivation by awarding bonus points based on your average monthly balance, helping those who struggle to save on their own achieve their goals.

In essence, BNPL is a service that "quickly fulfills the desire to have something," while SNPL is a service that "encompasses the purchasing experience of saving through one's own efforts to fulfill desires."

The Continuous Consumption Cycle Guided by SNPL

Next, we'll delve deeper into SNPL's benefits from the perspective of "customer engagement."

Did you know that Japanese department stores have long offered services similar to SNPL? The "Friends Club" service, said to have begun in the Taisho era, is a savings program implemented by many major department stores. For example, if you save a set amount for 12 months, you receive shopping vouchers or similar rewards at maturity, including a bonus equivalent to one month's savings. In the sense that saving a certain amount earns you a bonus, SNPL could be considered a modern version of the Friends Club service.

So, what significance does focusing on the experience of "saving to buy" rather than "buying now" hold for both consumers and businesses? Consumers using SNPL can not only ensure they purchase their desired items but also gain bonuses. Furthermore, having a clear goal makes saving easier to sustain compared to vague saving. It also fosters anticipation while waiting to obtain the product and provides a sense of accomplishment upon reaching the goal.

For businesses, SNPL holds the potential to foster long-term customer relationships. If a customer can purchase an item immediately, the relationship might end right then. However, with SNPL, the relationship with the customer is maintained throughout the savings period. Furthermore, businesses gain the advantage of utilizing data like user purchasing trends and income status for inventory management and marketing. In this way, SNPL can be considered a service offering significant benefits for both parties.

While SNPL may appear at first glance to be a service built on new technology, its core mechanism of "saving" is something deeply familiar to us. It represents a new service model that reconstructs existing concepts and systems using current technology and infrastructure. In a sense, it could be described as a service returning to the fundamentals of the consumer experience. This perspective could potentially be applied to other fields as well.

For example, an automaker could offer a "savings service enabling customers to purchase the latest luxury imported car set to launch in five years." Customers could save while looking forward to acquiring that car in five years. "Gaining motivation to continue saving for the future" and "the benefit awaiting at the end of the savings period" would make the experience more special, potentially enhancing engagement through increased trust and a sense of closeness toward the manufacturer.

While consumption styles like BNPL allow immediate purchase or experience of desired items, SNPL deliberately adopts a method that requires a longer timeframe to complete. This may seem inconvenient at first glance, but by setting benefits that feel valuable precisely because of the extended time invested, it holds the potential to deliver a superior experience. Furthermore, SNPL can foster long-term relationships with customers. Such service design and the building of trust with customers could offer valuable insights not just for SNPL, but for various businesses.

The information published at this time is as follows.

Was this article helpful?

Share this article