Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

The Power of Online Split Payments to Eliminate Negative "Organizer Troubles"

Yosuke Shibuya

SMILABLE Inc.

Toshiaki Hasamura

Dentsu Inc.

The benefits of fintech extend beyond corporations to individuals. Fintech services enabling easy "online split payments" for money exchanges among friends—like meals, gifts, or chartered boat parties—are gaining attention.

What is "Friend Funding," distinct from crowdfunding? How is fintech transforming marketing? FINOLAB Inc. hosted an interview with Yosuke Shibuya, CEO of SMILABLE, and Toshiaki Hasamura of Dentsu Inc. Business Creation Center.

Solving the negative "common organizer struggles": last-minute cancellations, advance payments, unpaid bills

Hasumura: When I learned about SMILABLE's service " I'm In," which enables online split payments among friends, I genuinely thought, "I wish I'd found this sooner." Could you first tell us about "I'm In"?

Shibuya: It's a service that helps you collect money online from your friends to make plans happen, like "Let's have a barbecue" or "Let's rent a private boat."

Whether it's dinners, class reunions, cherry blossom viewing, Halloween or year-end parties, gifts for birthdays or baby showers, or making team T-shirts for social clubs – whenever friends gather, money changes hands.

With "I'm In," you simply create your plan online, set your target amount and payment amount, then share it with your friends via SNS or email. There are no fees, and you can start in as little as 3 minutes.

Hasumura: For things like dinner parties, the organizer often collects cash to settle the bill. But with large groups, you might end up handling a lot of cash, which can be nerve-wracking.

Then there's the issue of last-minute cancellations or people leaving early. The organizer pays upfront, but then struggles to track down the person to get the money back... (laughs).

Shibuya: That's a classic organizer struggle. I'm the type who plans things thinking, "Let's all do something fun together!" so I totally get how organizers can get anxious about all sorts of things. It's no exaggeration to say I created this service to solve my own problems (laughs).

And it's not just about the money—I also dread the reactions when I ask, "Wanna do this?" What if nobody shows up? What if someone says "Yes" but then backs out later? Facebook events have those "Interested" or "Maybe" options, and I always think, "So what does that even mean?"

Hasumura: Since no money changes hands before attending, you do get those noncommittal responses, right?

Shibuya: Exactly. But with "I'm In," you can pay by card right when you confirm attendance, so last-minute cancellations tend to drop. Money only gets transferred to the organizer's bank account once the goal is met, so participants don't have to worry about "What happens to the money if the event doesn't happen?"

"I'm in." means "I'll participate." Shibuya explains, "We valued the image of participants gathering around the person who launched the plan, saying 'Me too!' or 'I'm joining!'"

The trend is shifting toward "experience consumption"—sharing experiences within communities.

Shibuya: I personally experienced an unexpected benefit while using "I'm in." Last year, I organized a plan to charter a yakatabune boat, and participants took the initiative to get involved.

You can't charter a yakatabune unless you have a large group, and the cost is high at around ¥10,000 per person. But because it was prepaid, there were zero no-shows or latecomers. What's more, some participants even invited their own friends, saying, 'I want to make this happen and enjoy it.' Since there was no money changing hands on the day, the organizer had no worries and could thoroughly enjoy themselves.

Mr. Shibuya and his friends planned and executed a private chartered houseboat for cherry blossom viewing

Hasumura: The concept of everyone pooling money for a specific purpose is similar to crowdfunding, which raises funds from a large, unspecified group of people. What is "I'm In" positioned as?

Shibuya: Crowdfunding often involves individuals contributing ¥10,000 or more to raise hundreds of millions of yen in total. "I'm In," however, is suited for smaller transactions like ¥300 or ¥1,000 per person, totaling around ¥10,000.

Similar C2C services exist overseas. Depending on the amount raised and the nature of the relationships among members, they're called group funding, community funding, or friend funding.

For example, in the US, there's an online payment service called " Venmo." It's very familiar to young people there. When friends go out to eat and someone pays for everyone, they might say, "Venmo me later!"

Hasumura: If friend funding mechanisms take hold in Japan, it could transform economic activity within communities.

Looking back at marketing trends, since the 21st century, consumption has shifted from focusing on material goods to prioritizing experiences. Furthermore, in recent years, there's been a shift from individual-centered experiential consumption to a preference for sharing experiences within one's community, such as with family, friends, or colleagues.

At the global event "FinSum: Fintech Summit" in September, Deputy Prime Minister Taro Aso, who was a speaker, also mentioned, "Nowadays, when young people split the bill, they can use their smartphones for electronic payments." This service fits perfectly with recent trends.

Shibuya: Thank you. I also had the opportunity to speak at FinSum's pitch competition (PITCH RUN), so I was very pleased to hear Deputy Prime Minister Aso's remarks directly at the venue.

"I'm In" is essentially entertainment-focused fintech. There are plenty of fun ideas out there, but often they don't materialize because of hurdles like "this plan would require too much upfront spending..." or other practical difficulties.

I feel that by dramatically lowering these barriers with technology, we can promote more enjoyable consumption within communities.

Hasumura: I can envision "I'm In" acting as a lubricant, helping to uncover fun and interesting activities, boosting sales, and creating a well-functioning cycle within the market itself.

Shibuya: Our goal is for people to recognize that wherever a community exists, "I'm In" is there too. We want to permeate to the position of being the most accessible fintech for people, eliminating the negative aspects of community activities and supporting happy relationships.

Contributing to regional revitalization at the community level

Hasumura:Starting in October, we began a collaboration with " Okurimono Sommelier," a new proposal-based gift site launched by 47CLUB Inc. (Yon-nan Club), which operates a mail-order site featuring products carefully selected by local newspapers nationwide.

Okurimono Sommelier, the platform for this collaboration, is a proposal-based gift site that recommends the "perfect" gift to delight the recipient simply by selecting their preferences and lifestyle. With many regional specialties featured, it seems like a very interesting initiative that could also serve as an effective function for regional revitalization.

Shibuya: Mr. Hasamura introduced us to 47CLUB Inc., leading to this collaboration. With the year-end gift season and Christmas party season approaching, we hope to see increased demand for group purchases (where friends pool money to buy gifts).

For example, to host a slightly more luxurious year-end party, you could pool funds via "I'm In" to order premium wagyu beef.

Another fun approach is setting a budget but not splitting evenly. Instead, set the payment amount to "any amount is OK," then buy quality meat or premium alcohol based on the total collected. People might say, "I plan to drink a lot, so I'll put in ¥10,000!" or "I'll join late, so ¥3,000." Deliberately not fixing the amount creates a different kind of enjoyment within the community.

Hasumura: If demand expands by effectively using these delivery sites at the community level rather than individually, it could become a new style of regional revitalization.

Visualizing the flow of money will further evolve marketing

Hasumura: How do you think fintech can contribute to the community economy?

Shibuya: Traditionally, money transfers involved cash handovers for nearby transactions and costly methods like cash-on-delivery or bank transfers for distant parties.

However, fintech services enabling card payments not only eliminate the barrier of fees but also transcend currency barriers, allowing transactions across national borders.

Hasumura: So it means the community economy will extend beyond domestic borders to include overseas friends as well.

Shibuya: Exactly. The concept of community economy will evolve to encompass globalization. For instance, what was primarily domestic consumption—like city dwellers buying pesticide-free vegetables from rural farmers—will increasingly involve people living in China or other countries purchasing Japanese products locally. This could significantly boost income for rural areas.

Hasumura: That said, Japan still heavily relies on cash. You're trying to bring about a paradigm shift there, aren't you?

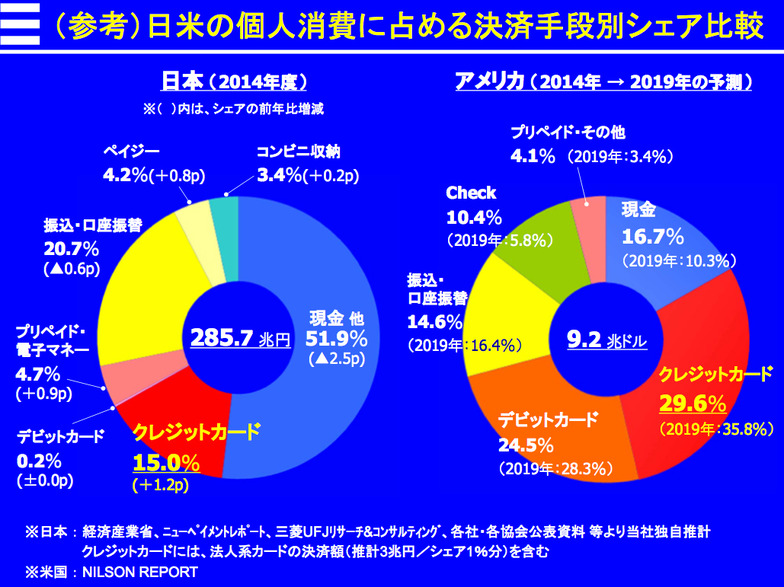

Shibuya: That's right. Cash still accounts for about 50% of personal consumption payments in Japan, a higher proportion than in the US, where cash payments are below 20%. In the US, some projections suggest cash payments could drop to around 10% by 2019.

Shibuya: With the Tokyo 2020 Olympics and Paralympics approaching, Japan is also expected to see increased cashless adoption going forward. Furthermore, accelerating cashless payments will reveal many new possibilities.

For example, suppose I buy beef with Mr. Hasamura splitting the cost, and he pays for it upfront. If I give Mr. Hasamura cash, no payment history remains, right?

But with "I'm In," data remains showing how much I paid Mr. Hasamura and for what purpose, which becomes marketing information. Previously, companies could only see information about the representative who made the payment. Now, deeper insights become visible—like how many people contributed and how much each paid toward the purchase.

Hasumura: This big data captures C to C transactions that were previously invisible, linking them to their purpose, revealing real insights.

Shibuya: That's right. In the future, we plan to offer services handling such big data and incorporate various payment methods beyond credit cards, including point-based payments.

Hasumura: Thank you very much.

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Back Numbers

Author

Yosuke Shibuya

SMILABLE Inc.

President and CEO

Born in 1979. Joined Ogilvy & Mather, a foreign-affiliated advertising agency group, in 2004. Worked as a systems engineer, producer, and planner on online marketing for domestic and international clients. Subsequently served as E-commerce Manager at TaylorMade Golf. In 2014, founded SMILABLE, which provides online business planning, development, and operations, as well as crowdfunding services.

Toshiaki Hasamura

Dentsu Inc.

Business Development & Activation Division

During my student years, I incorporated a photography business (started a company). I covered approximately 40 countries. Subsequently, I joined Dentsu Inc. with the goal of launching a social business within an organization capable of significant social impact. While working on new business development led by Dentsu Inc., I also engaged in PRE/PFI consulting, such as advisory services for PFI concession bidding projects like airport privatization, and consulting for new commercial facility development project planning. Examples of business development include: - 2013: Conceived and participated in launching Japan's first crowdfunded mass media broadcast project, "LISTENERS' POWER PROGRAM." - 2016: Conceived and participated in establishing Japan's first FinTech industry hub, The FinTech Center of Tokyo "FINOLAB Inc.", where I remain active daily as part of the operational team. - 2018: Left Dentsu Inc.