Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

Electronic bonds for difficult financial procurement. Fintech will save the construction industry!

Aki Kaihori

Ministry of Land, Infrastructure, Transport and Tourism

Takashi Ogura

Tranzax Co., Ltd.

Izumi Ogoshi

Dentsu Inc.

FinTech, a portmanteau of finance and technology, represents the power to transform society. It enables anyone, anywhere, to benefit from convenient financial services through the power of technology.

This episode's theme is "Can FinTech Save the Construction Industry?"

Japan has approximately 460,000 construction companies, 99.4% of which are small and medium-sized enterprises. Regarding the financial challenges of the construction industry, known for its heavy use of promissory notes and difficult cash flow, discussions were held with Mr. Yasuki Kaihori, Director-General for Construction and Distribution Policy at the Ministry of Land, Infrastructure, Transport and Tourism; Mr. Takashi Ogura, President of Tranzax, which developed a new financing scheme utilizing electronically recorded monetary claims*; and Ms. Izumi Ogoshi, Director of DENTSU SOKEN INC.

※Electronic Recorded Monetary Claims: A new type of monetary claim created to improve the cumbersome procedures and security issues associated with traditional bills and accounts receivable, facilitating smoother financial procurement. They can be processed instantly via the internet.

Deputy Director General Kaibori of the Ministry of Land, Infrastructure, Transport and Tourism (center), President Ogura of Tranzax (right), Director Ogoshi of DENTSU SOKEN INC. (left)

SMEs can obtain financing based on the "creditworthiness" of their ordering companies

Ogoshi: Tranzax, also a tenant at FINOLAB Inc., is a fintech company utilizing electronic recorded claims. What led you to focus on this business?

Ogura: I originally worked at a securities firm. The financial industry that nurtured me is now stagnant. Finance is about "facilitating the flow of funds," yet the mainstream systems haven't fundamentally changed.

While developing businesses at various companies, I realized that services addressing societal problems could evolve into sustainable ventures. That's why I started this business, aiming to contribute to society through electronic recorded receivables that help SMEs manage their cash flow.

The " Supply Chain Finance " initiative, designated by the government in July 2016, is based on the concept of "optimizing finance by looking at the entire supply chain involved in product manufacturing."

Using this service can streamline financing compared to separate planning by stakeholders. Suppliers (both suppliers and purchasers) can potentially secure funding under favorable interest rate terms based on the primary manufacturer's (the ordering company's) creditworthiness, regardless of their own credit standing.

Interest rates for SMEs are high, and discount rates for bills of exchange are also high.

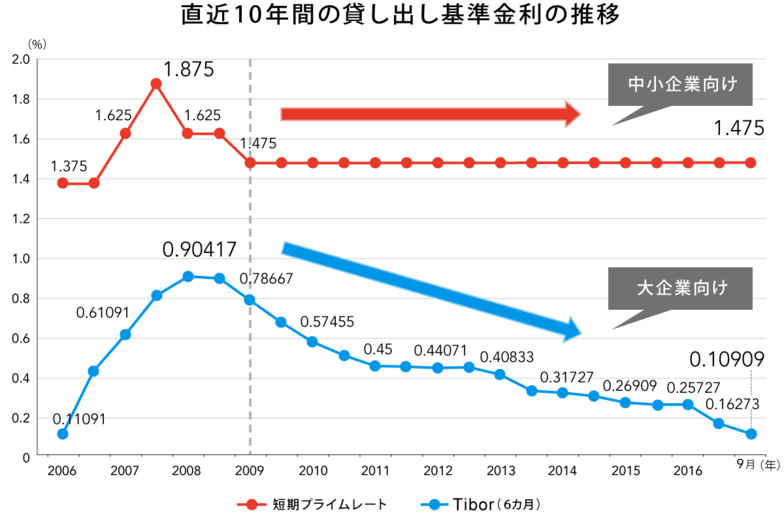

Ogura: In Japan's interest rate market, the benchmark rate (Tibor) for large corporations' financing has been steadily declining. However, the benchmark rate (short-term prime rate) for SMEs' financing has remained high for the past seven years, creating a 13.5-fold difference.

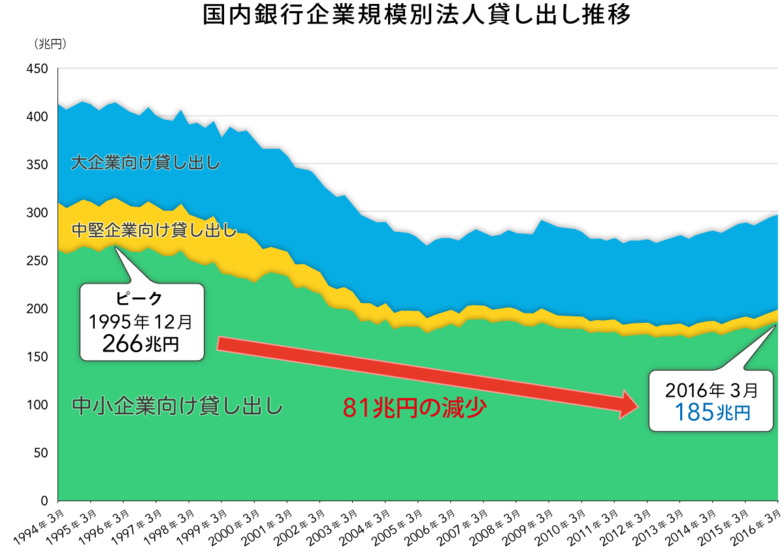

Ogura: Furthermore, lending to SMEs has significantly decreased from its peak of ¥266 trillion in 1995 to ¥185 trillion in 2016 (Bank of Japan survey). I believe the reason the benefits of Abenomics haven't reached SMEs is because there was no mechanism to ensure they did.

Kaibori: The biggest problem remains that financial institutions cannot accept collateral other than real estate, or rather, they cannot properly evaluate it.

In the construction industry, for private projects, payment terms can be extremely harsh. Examples include typhoon bills, where payment takes about seven months, and ten-ten-pa bills (10:10:80), where 10% of the contract amount is paid at commencement, 10% at the roof-raising stage, and the remaining 80% upon completion.

Ogura: The reality is that construction companies have been managing their finances through bill discounting*. Since discount rates depend on the company's creditworthiness, construction firms without collateral or those with prior-year losses face extremely harsh discount rates on their bills. When a client company issues bills with such strict discount rates, the impact ripples down to primary and secondary subcontractors.

The advantage of this "supply chain finance" is that it is evaluated based on the client's creditworthiness. It effectively leverages the creditworthiness of the primary ordering party rather than just the contractor receiving the order. Furthermore, using electronically recorded claims makes it very low-cost and simple, reducing administrative burden.

※Bill discounting... The practice of selling a promissory note to a bank or other financial institution before its due date, receiving payment minus an amount equivalent to interest.

Oogoe: This is truly groundbreaking for the overall financial health of the construction industry.

If purchase orders become collateral, could this inject vitality into regional areas!?

Ogura: Actually, before founding the company, I visited regional banks and prefectural offices nationwide aiming for regional revitalization, learning about local economic challenges. For regional areas, the construction industry is undoubtedly a major backbone industry. The further you go into the regions, the fewer large companies exist outside of construction.

On the other hand, construction is a business model inherently prone to cash flow difficulties, where money goes out upfront for things like procuring building materials, and payment is received later from the purchaser. If construction companies go bankrupt due to reluctance to lend, it becomes an employment problem and could develop into a serious issue for the regional economy.

Ogure: So, the challenge is that while we want to prevent the regional economy from deteriorating, financial institutions have few effective methods for providing loans?

Ogura: In the early 2000s, the Financial Services Agency's inspection manual classified loans to loss-making companies as non-performing assets the moment they were made. If a local loss-making company secured a good project and a lender wanted to finance it, they would need to set aside loan loss provisions.

This raises the question: Is it acceptable for private companies, as profit-seeking entities, to make loans that require setting aside loan loss provisions from the outset? It amounts to a breach of fiduciary duty to shareholders. It's problematic to proceed knowing there will be losses, and I believe this has left them unable to act.

Ogure: Listening to President Ogura now, it seems the fundamental challenge moving forward is establishing the basis for financial institutions to operate, such as providing collateral.

Ogura: I agree. In fact, we are actively considering applying for approval for a new service called "PO Finance." This mechanism allows financial institutions to use purchase orders (POs) as collateral by registering them as conditional electronic claims.

Ogoshi: It's reassuring that financial institutions can provide funding right from the order placement stage.

Kaibori: In the construction industry, public works projects are leading the way. They use a system where public entities provide guarantees through guarantee institutions and pay "advance payments" to the relevant companies.

Ogura: With PO financing, the key issue will likely be determining at which stage and in what form the debt transactions occur. By addressing this properly, we believe similar financing could be extended to private projects as well.

Just reducing the burden of securing financing allows companies to move forward proactively.

Ogoshi: When the president visited various regions before founding the company, was the primary need he identified financing starting from the order placement stage?

Ogura: Yes. In private construction projects across different regions, for example, undertaking large projects like apartment building construction, a single order could exceed half of the company's previous year's sales. That inevitably leads to insufficient working capital.

Ogami: Even though they secured a major project...

Ogura: Statistically, regional banks only lend one-third of their total loans without collateral or guarantees. So, if there were a system where companies could borrow money based on their order forms, they'd strive to win big contracts. This would allow companies to grow, open up various opportunities, and inject vitality into the Japanese economy as a whole.

Kaibori: Many construction companies do solid work but lack financial procurement capabilities. It would be ideal if the client themselves could verify the company's work quality and decide, "Let's go with this company." Eliminating cash flow struggles would allow companies to focus solely on construction. They could then concentrate on quality assurance and sales efforts.

Within a single supply chain, when a client assigns work to a company, this mechanism allows the client to manage how much financial capacity or credit line to extend based on a certain level of work progress. This means the project can be managed using the client's financial strength, creditworthiness, and procurement power, rather than relying solely on the contractor's financial resources, credit, or funding ability. Consequently, I believe the client's overall financial costs could decrease.

Ogura: It's a forward-thinking mechanism that effectively utilizes the contractual relationship between the ordering party and the recipient. It enables low-cost, effective financing and leads to quality improvements and innovations in various areas, such as enhancing on-site productivity.

Filling the gaps in business with technology and ingenuity

Ogoshi: I apologize for asking something a bit blunt, but construction falls under the Ministry of Land, Infrastructure, Transport and Tourism; fintech under the Financial Services Agency (Ministry of Finance); and SME support under the Small and Medium Enterprise Agency (Ministry of Economy, Trade and Industry). Being caught between multiple ministries, is there an aspect where public support takes time to reach?

Kaibori: I understand your point, but I think the approach is different. When a crisis hits, everyone pitches in to fill the gaps.

For example, immediately after the Lehman Shock, the Small and Medium Enterprise Agency spearheaded a safety net initiative using credit guarantee associations. This included 100% financing and 100% guarantees for SMEs. For the construction and real estate sectors, we lobbied various parties to raise the standard 80% guarantee under the safety net to 100%. I believe Japan's strength lies in its ability to respond swiftly and smoothly through coordinated efforts during crises.

However, when the economy improves, we can't intervene in matters that private companies can handle themselves. It's a free world of private enterprise, so unless someone in the private sector throws a new pitch in the market, government agencies can't just come up with ideas and push them forward.

Oogoe: What about from the perspective of eliminating entrenched regulations or breaking down constraints?

Kaibori: If regulations exist, we can break through the constraints, but filling the white space is difficult. However, when trouble arises, we collaborate to respond. Mortgage-backed securities* might be a good example.

Historically, the pattern has been to tighten regulations and patch things up when problems occur. In sectors like construction and real estate finance, mechanisms like real estate collateral and pledge collateral are already established, with meticulous procedures designed to prevent trouble. Consequently, there was an aspect where attempts to simplify and utilize them at the practical level didn't gain traction.

※Mortgage-backed securities: Financial products created by securitizing small portions of mortgage rights on real estate like land and buildings. The Mortgage-Backed Securities Act of 1931 enabled lending using these securities as collateral. However, issues like empty issuance arose during the bubble economy, leading to tighter regulations. The Mortgage-Backed Securities Business Act was enacted in 1987 (now consolidated into the Financial Instruments and Exchange Act).

Ogura: We aim to provide solutions that simplify commercial transactions across various fields by leveraging new technologies like fintech or electronic recorded claims.

Kaibori: The fintech field is, in a sense, a blank canvas. I think it's groundbreaking for private companies to apply ingenuity to this blank canvas in business, proposing and filling in that blank space as a business model.

Ogoshi: Fundamentally, new technologies like fintech hold the potential to become simpler and more convenient the more people use them. For instance, while "electronically recorded claims" is the precise term, we might need to work on replacing it with more accessible language.

Kaibori: That's probably true. When discussing financial terms or procedures with people in the construction industry, they might be completely baffled. Trying to write about procedures or legal regulations accurately can become complicated. I think it's crucial to leverage fintech technology, simplify things after thorough review by relevant parties, and then disseminate them widely.

The financial sector is particularly difficult. That's precisely why I believe the most important thing is to properly disseminate complex financial concepts to a wide audience using clear, accessible language and a flexible approach. In advancing this kind of public relations effort, we have high expectations for Dentsu Inc.

Ogura: We look forward to your support. Likewise (laughs).

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Back Numbers

Author

Aki Kaihori

Ministry of Land, Infrastructure, Transport and Tourism

Director-General for Construction and Distribution Policy, Minister's Secretariat

Born in 1961 in Hyogo Prefecture. Joined the Ministry of Construction in 1984. Held positions including Director of the Real Estate Industry Division at the Ministry of Land, Infrastructure, Transport and Tourism (MLIT), Director of the Corporate Planning Office at the Urban Renaissance Agency, Senior Advisor to the Director-General at the Reconstruction Agency, and Deputy Director-General of the Minister's Secretariat at MLIT. Assumed current position in July 2015.

Takashi Ogura

Tranzax Co., Ltd.

President and CEO

Born in 1963 in Tokyo. Joined Nomura Securities in 1986. Worked in structured finance within the Financial Institutions Department before handling management planning in the Accounting Department. Served as Executive Officer and Head of Corporate Planning at FM Tokyo and Executive Officer at CSK-IS. Founded Tranzax in July 2009 and assumed the position of Representative Director.

Izumi Ogoshi

Dentsu Inc.

Dentsu Inc. Innovation Initiative

Executive Business Creation Director (EBD)/Legacy Project Design Office Manager

After working at a think tank and a foreign-affiliated manufacturer, joined Dentsu Inc. in 1998. Served in the Marketing Bureau, Communication Design Center, and Business Design Lab before assuming current position in 2014. Aims to accelerate innovation triggered by 2020 & Beyond, engaging in domestic and international business strategy and brand communication strategy for client companies.