Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

The new customer journey born from the digital shift during the pandemic

The impact of the novel coronavirus has reached the fashion industry, but the effect on luxury brands has been particularly significant. Coincidentally, this has coincided with a growing call to reexamine longstanding business practices and culture, becoming a distant cause of what can truly be called a Great Reset(※) – a tectonic shift.

※ = The Great Reset

A concept advocating the redefinition of capitalism and a comprehensive rethinking of the current global economic system. It was also the theme of the 2021 World Economic Forum.

In response, Dentsu Inc., The Goal Inc., and Condé Nast Japan launched a joint research project to investigate the impact of the pandemic on luxury brand business. They conducted a detailed analysis of changes in media engagement and purchasing behavior among the younger generation, known as Generation Z, who represent the future customer base.

This series reports on the findings. Furthermore, it examines major trends like the "Great Reset" in the luxury industry and the momentum behind the SDGs to illuminate the future path for luxury brands.

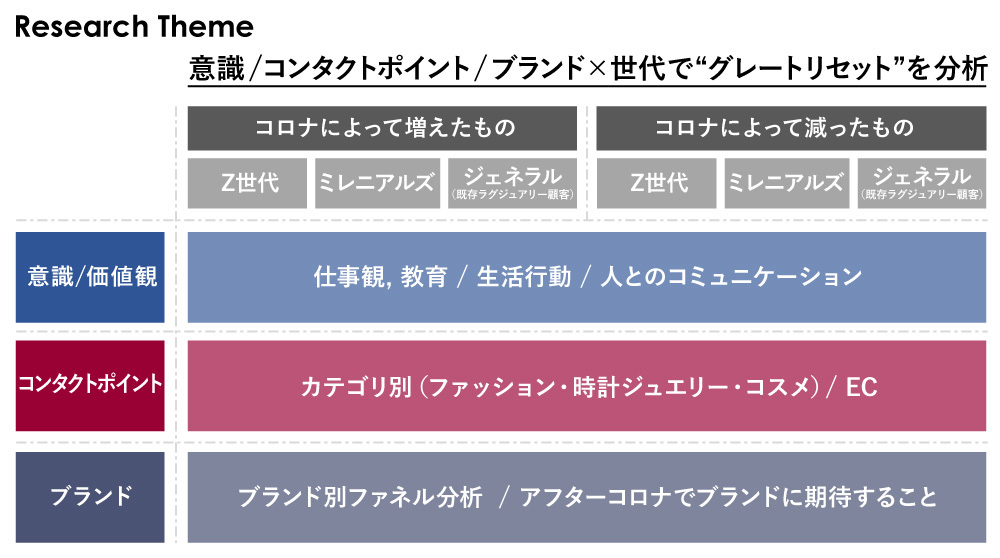

The survey utilized a combined panel from Condé Nast Japan and Dentsu Macromill Insight, Inc., targeting fashion-conscious women divided into three generations: Generation Z (24 years old and under), Millennials (25-39 years old), and General (existing buyers, 35 years old and over).

For each generation, the survey employed a multidimensional approach combining "Generation × Values," "Generation × Contact Points," and "Generation × Brands," further examining "Existing Attitudes" alongside "Changes Due to COVID-19" (increases and decreases). The research comprised both quantitative surveys via questionnaires and qualitative interviews.

This first installment focuses on introducing the "Generation × Contact Point" aspect.

The survey design presented respondents with over 20 contact point options categorized by type, such as "TV," "Magazines," "SNS," "In-store," and "Friends." Furthermore, for respondents who selected "SNS," we provided over 15 detailed follow-up options—such as whether it was "Brand Official LINE," "Celebrity Influencer Instagram," or "Micro-Influencer Twitter"—to enable a more concrete understanding of actual behaviors.

Contact Points by Category. SNS Use Increased During the Pandemic

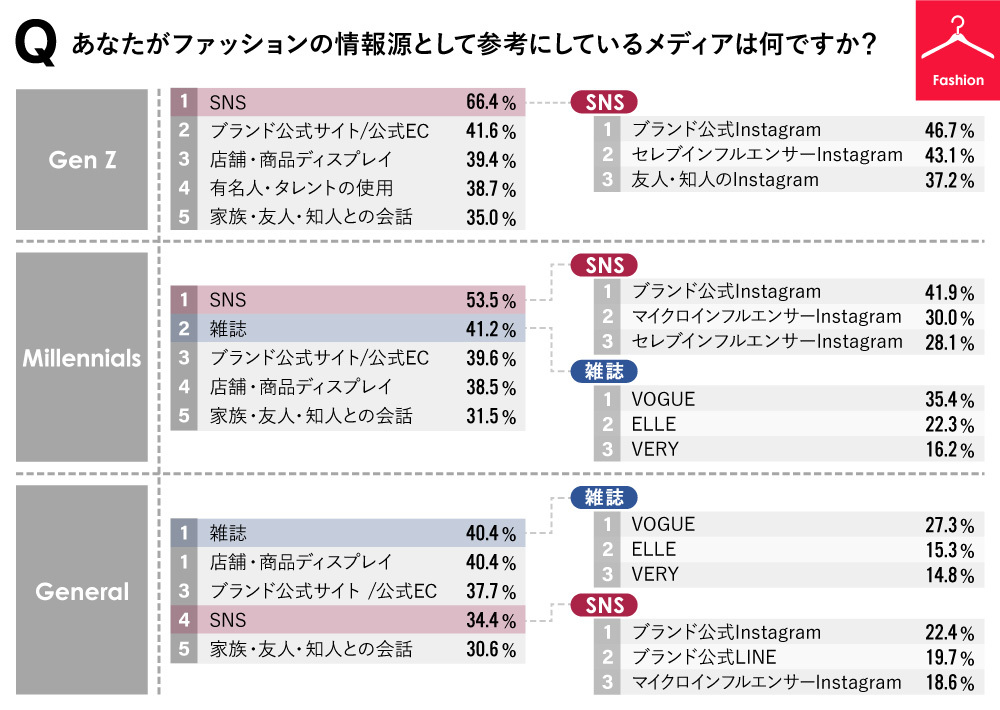

First, the results for information sources referenced in the fashion category are as follows.

The influence of SNS is stronger among younger demographics, with Instagram holding significant sway for both Gen Z and Millennials. However, preferred influencers show generational characteristics, shifting from "Celebrity Influencer Instagram" to "Micro-Influencer Instagram" as age increases.

This reveals a category characteristic: younger consumers reference media driven by "admiration for items worn by that celebrity." As they age and establish their own style, the tendency shifts toward "referencing fashion by observing shop staff, etc."

Additionally, for Millennials and older demographics, "magazines" and "physical stores" exert strong influence, serving as effective touchpoints, particularly for existing luxury customers aged 35 and above.

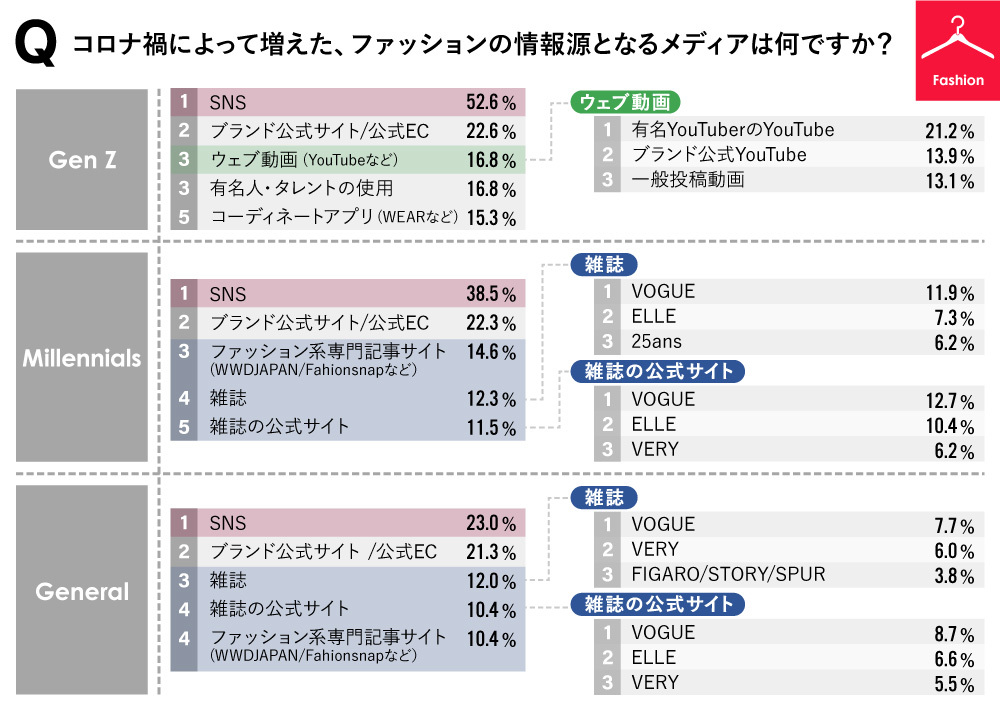

Next, the sources of fashion information that increased due to the pandemic are as follows.

The media that increased across all generations was "SNS." A notable characteristic is that Gen Z shows heightened interest in video content, while Millennials demonstrate increased interest in high-end fashion media, regardless of whether it's magazines or web-based.

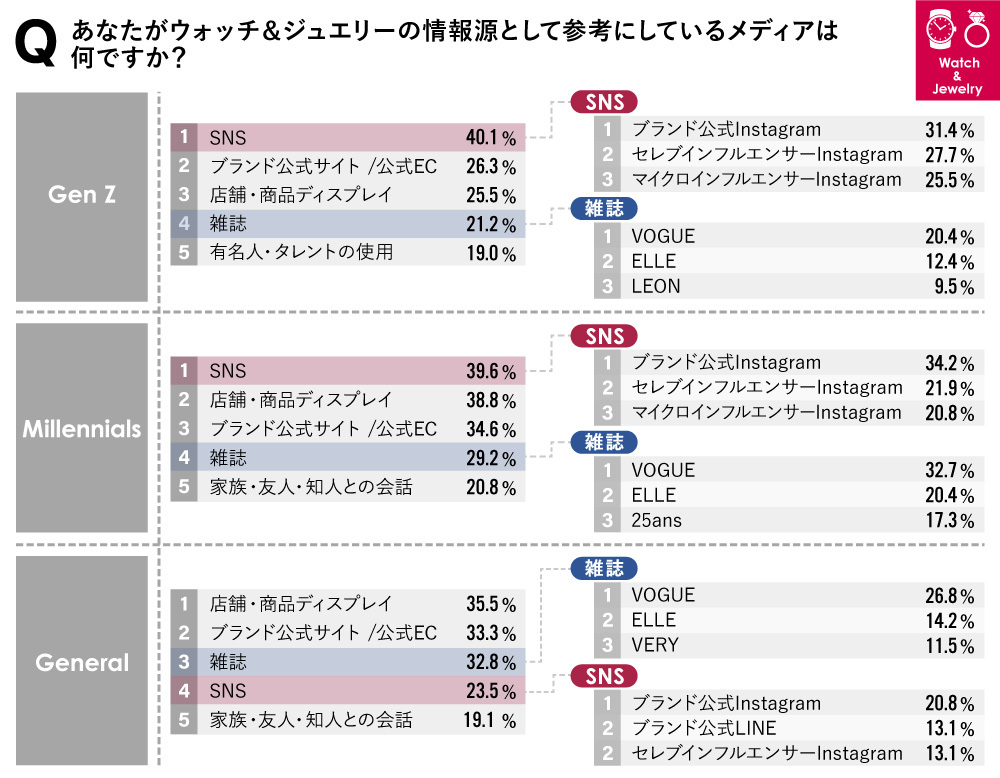

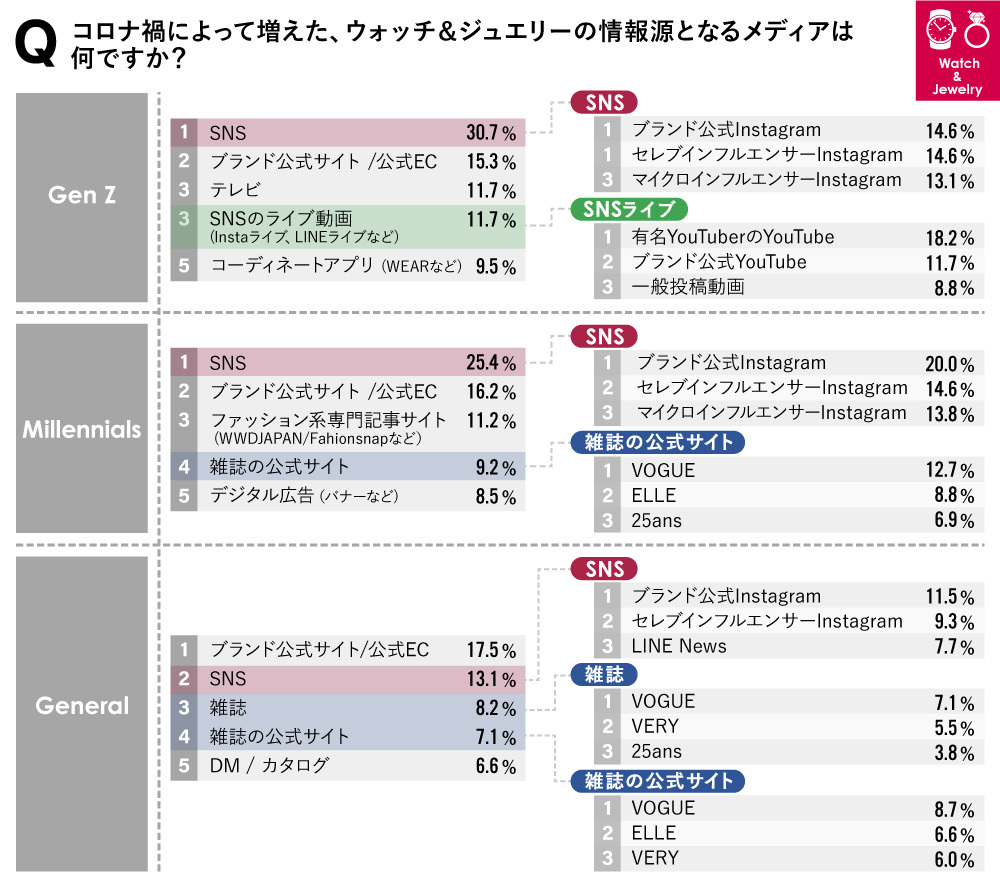

Next, regarding contact points for the Watch & Jewelry (W&J) category. Here too, SNS (Instagram) holds significant influence. Unlike fashion, this category features products with a stronger "aspiration" element, leading to a noticeable presence of celebrity influencers over micro-influencers across all generations. Another characteristic is the higher influence of magazines compared to the fashion category, observed across all age groups.

Next, regarding contact points that "increased due to COVID-19," Watch & Jewelry shows a trend similar to fashion: "SNS" was the medium that increased across all generations. Generational differences mirror fashion: Gen Z shows higher interest in video, while Millennials and older generations show greater interest in high-end media.

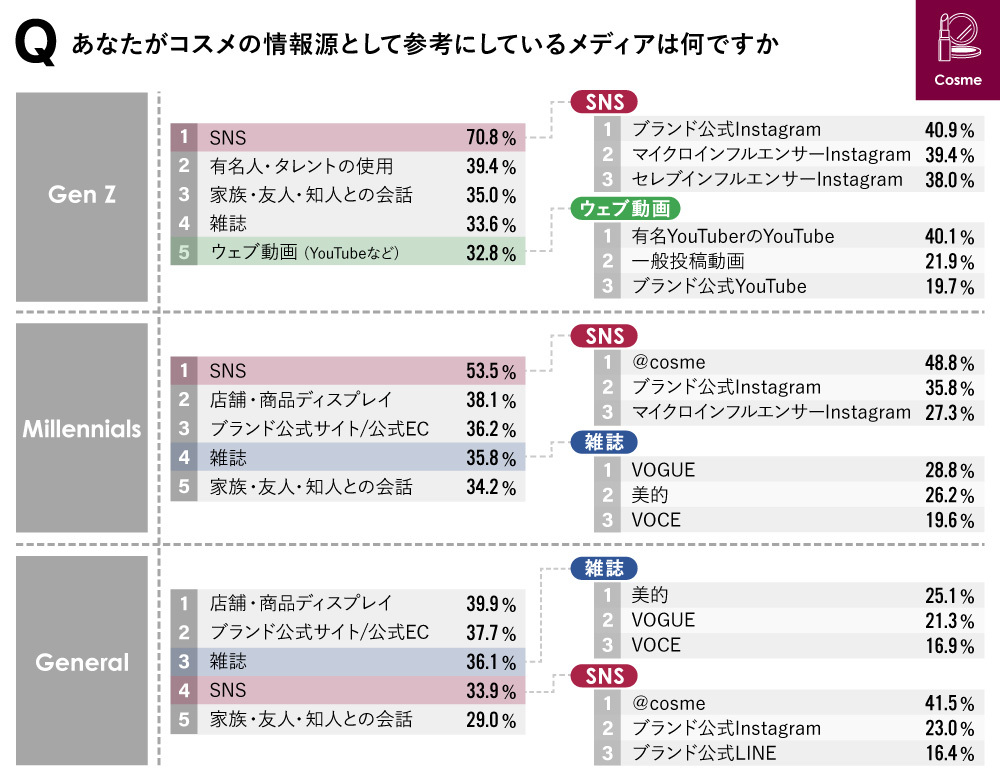

Next, we introduce contact points in the cosmetics category.

Overall, "SNS" scores high here too, but the specific SNS platforms differ by generation. While Gen Z favors "influencer campaigns on Instagram" and "popular YouTuber makeup videos," for Millennials and older, the top "SNS" is "@cosme," followed by "brand official Instagram." Another notable characteristic is a tendency for older age groups to prefer "official information" such as "in-store," "beauty magazines," and "brand official channels."

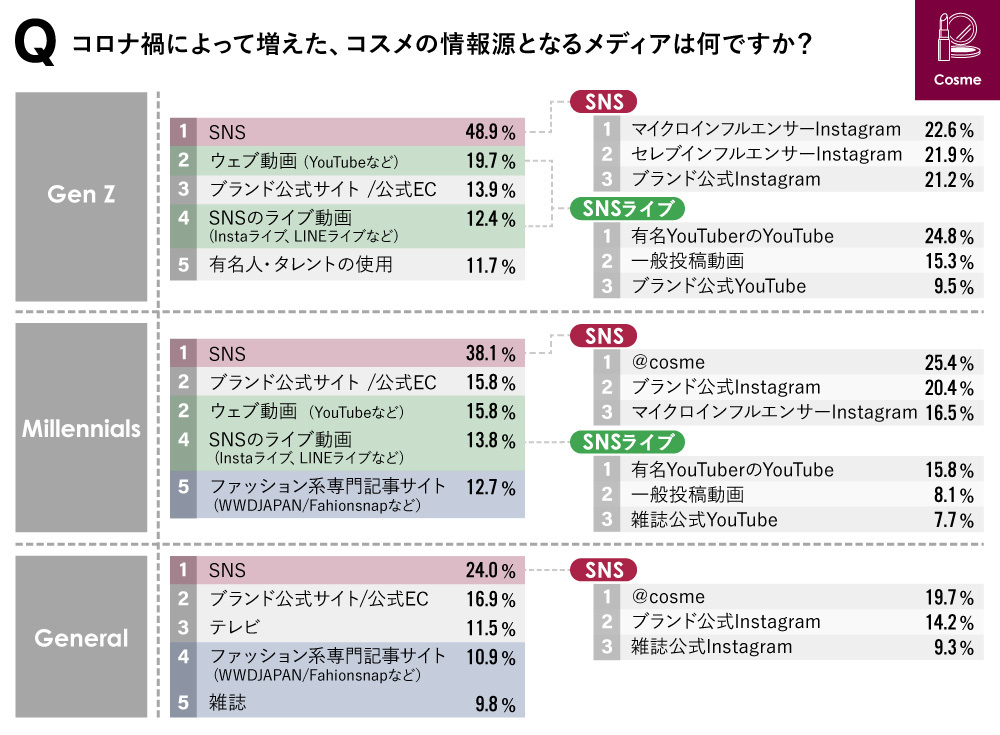

Meanwhile, media that saw growth during the pandemic include the surge in content like makeup videos by famous YouTubers and on SNS, which cosmetic brands implemented in 2020. @cosme, favored by Millennials and older generations, also showed growth.

Changing Contact Points and the New Customer Journey

Summarizing the above results yields the following insights.

"Contact points that decreased during the pandemic" included those requiring physical outings, such as "retail stores," "exhibitions/events," and "outdoor advertising," regardless of category.

While "SNS" stood out as the media that increased overall during the pandemic, its high score isn't solely due to "younger demographics." Though omitted in this series, the same survey conducted for the "automotive category" showed that even among younger consumers, TV, official websites, and online ads remained strong information sources. Therefore, the factor is likely the "high affinity between the Fashion/W&J/Cosmetics category and SNS" rather than "generational characteristics."

Considering these survey findings and shifts in the social environment, we will examine "post-pandemic contact points in the luxury category" ( ) and the "customer journey" alongside two key concepts.

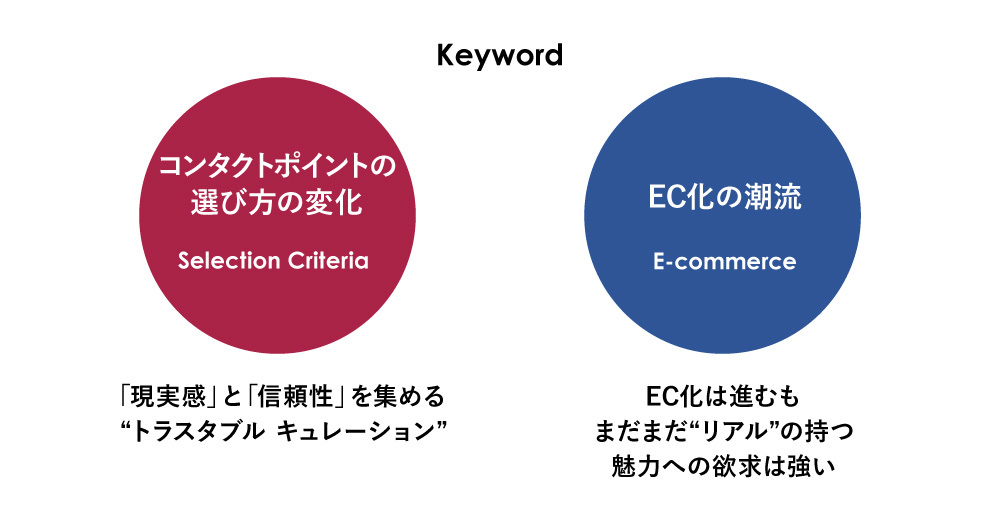

The accelerated digital shift has changed "how contact points are selected"

The first keyword is "changes in how contact points are selected." A major characteristic observed in the survey results was that the already strong support for "SNS" and "official content" (official websites, official SNS, authoritative magazine media, etc.) appears to have accelerated further during the pandemic.

Interviews also frequently revealed that people are "looking for trustworthy information above all else." As factors behind the increased support for SNS and official content,

"SNS offers Reality = tangible, real information that feels relatable to me"

"Official content provides Reliability—information from trustworthy sources."

This suggests that people are seeking "Reality" – tangible, real information that feels authentic to them – from

In other words, "Trustable Curation" (gathering what one personally trusts) defines engagement with contact points. Conversely, sources lacking either a sense of reality or reliability are expected to become less referenced as information sources.

Incidentally, this survey also categorized "trustworthy information sources." Younger demographics tend to trust "relatable individuals" like reviewers and social media users, while older age groups increasingly place trust in "reliable authorities" such as magazines and official websites.

E-commerce advances, yet desire for the real remains strong

The second keyword is the "trend toward e-commerce." While this is an irreversible trend across all categories, it still presents significant hurdles, particularly for luxury goods.

In this survey, traditional reasons like material feel, sizing, and actual color appearance ranked high among reasons for not purchasing online. Interviews also revealed:

"The foreign models wearing the items on the site lack realism for me, making it hard to visualize myself wearing them."

"Official e-commerce sites heavily retouch photos. I use platforms like Mercari, where amateur photos feel more real, to check if items I like match my expectations."

"I often end up seeing and buying items I discovered online in physical stores."

"Expectations for a special in-store experience"

These responses indicate that the desire for the appeal of the "real" remains strong, reflecting the current state of luxury e-commerce.

The Customer Journey Created by Trustable Curation

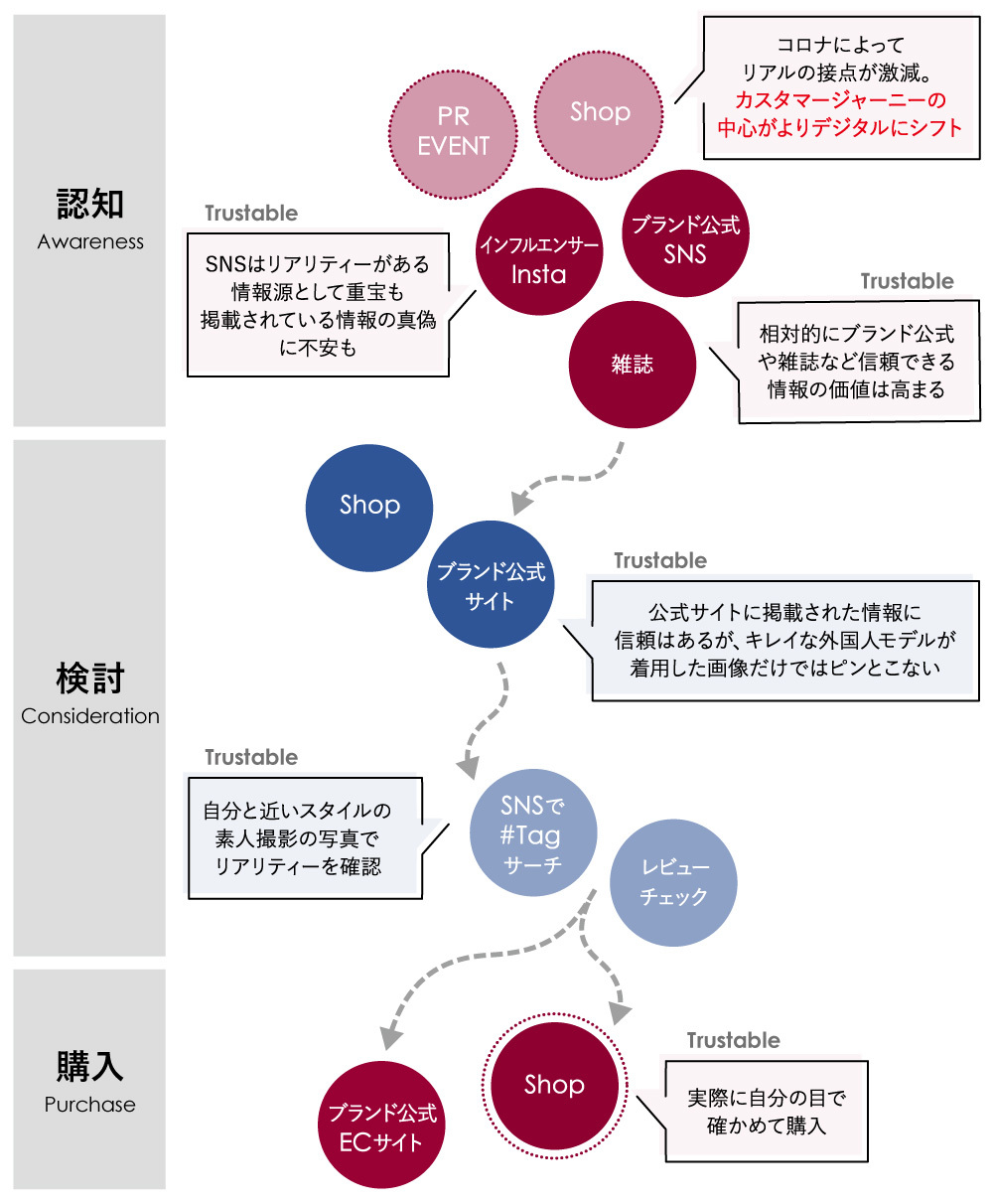

Based on these survey results and keywords, we're re-examining the customer journey. Abstracting the path from awareness to purchase yields the following structure.

Representative contact points in the awareness phase included official brand SNS, influencer SNS, magazines, physical stores, and events. However, the pandemic reduced real-world touchpoints like events and stores, shifting the core of the customer journey more strongly towards digital.

While SNS presence grew stronger, survey data also showed a trend where, perhaps as a reaction to excessive digital shift, contact points like official brand content and authoritative magazines gained increased value. This was to reinforce the "reliability of information" flowing digitally.

Next, the consideration phase. While this was once primarily the official website or physical stores, COVID-19 restrictions have reduced in-store opportunities, leading consumers to check products on official websites instead.

While the information found there is highly reliable, reasons like seeing foreign models wearing the items making it hard to relate personally or concerns about image retouching lead consumers to seek "reality" through SNS hashtag searches and review checks. Ultimately, the purchase phase involves selecting a physical store where the buying action occurs.

The survey results revealed this customer journey, aligning with what consumers perceive as "trustworthy."

When the internet first emerged, the term "showrooming" became popular, describing the behavior of "researching in-store and ultimately purchasing online," forcing many industries to adapt. However, the opposite phenomenon, which could be called "reverse showrooming" – "researching online and ultimately purchasing in-store" – has become the current customer journey in the luxury category.

Perhaps sensing this trend, a certain renowned luxury brand launched a "home try-on service" late last year. This service allows customers to select products on the official online shop and try them on at home free of charge—a concept once unthinkable in the luxury world.

Next time, we will discuss how brands should communicate information and what they should convey to consumers amid the pandemic, particularly as Gen Z's new values—seeking authenticity and trustworthiness—and the trend of "trustable curation" become established.

[Survey Overview]

Survey Title: "Post-COVID Luxury Brand Survey"

Conducted: September 2020

Research Method: Internet survey (quantitative) / Face-to-face interviews (qualitative)

Survey Participants: High-involvement luxury consumers, total 1,800 SS

Target Categories: Fashion / Watches & Jewelry (W&J) / Cosmetics / Automobiles

Research Firm: Dentsu Macromill Insight, Inc.

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Author

Yutaka Matsuda

Dentsu Inc.

Account Production Center

Communication Planner

After working at advertising agencies both in Japan and abroad, he joined Dentsu Inc. He has been involved in various media-related tasks, including contact point analysis, strategy development, effectiveness measurement, and campaign planning.