Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

How have climate change and inflation altered purchasing behavior? ―From the Sustainable Lifestyle Awareness Survey 2023―

Dentsu Inc. and DENTSU SOKEN INC. jointly conducted the third " Sustainable Lifestyle Survey 2023 " (hereafter SLS2023), following the 2021 survey ( survey overview here ).

The survey covered six countries: Japan and China from East Asia; France and Germany from Western Europe; and Indonesia and Thailand from Southeast Asia. While also referencing survey data from the United States (※1), the research team will interpret and analyze the results of this international survey. This time, we present several key topics focusing on the noteworthy theme of "Climate Change × Purchasing Behavior."

※1

Dentsu Group's North American survey "Dentsu Consumer Navigator: Sustainability 2023." SLS2023 aligned some survey items and target conditions with this survey.

<Table of Contents>

▼Climate Change Impacts: "Food and Water" and "Cost of Living." 2023 Saw Stealth Price Hikes Too

▼Refills for Daily Goods? Or Container Recycling?

▼Resistance to Avoiding Beef Decreasing

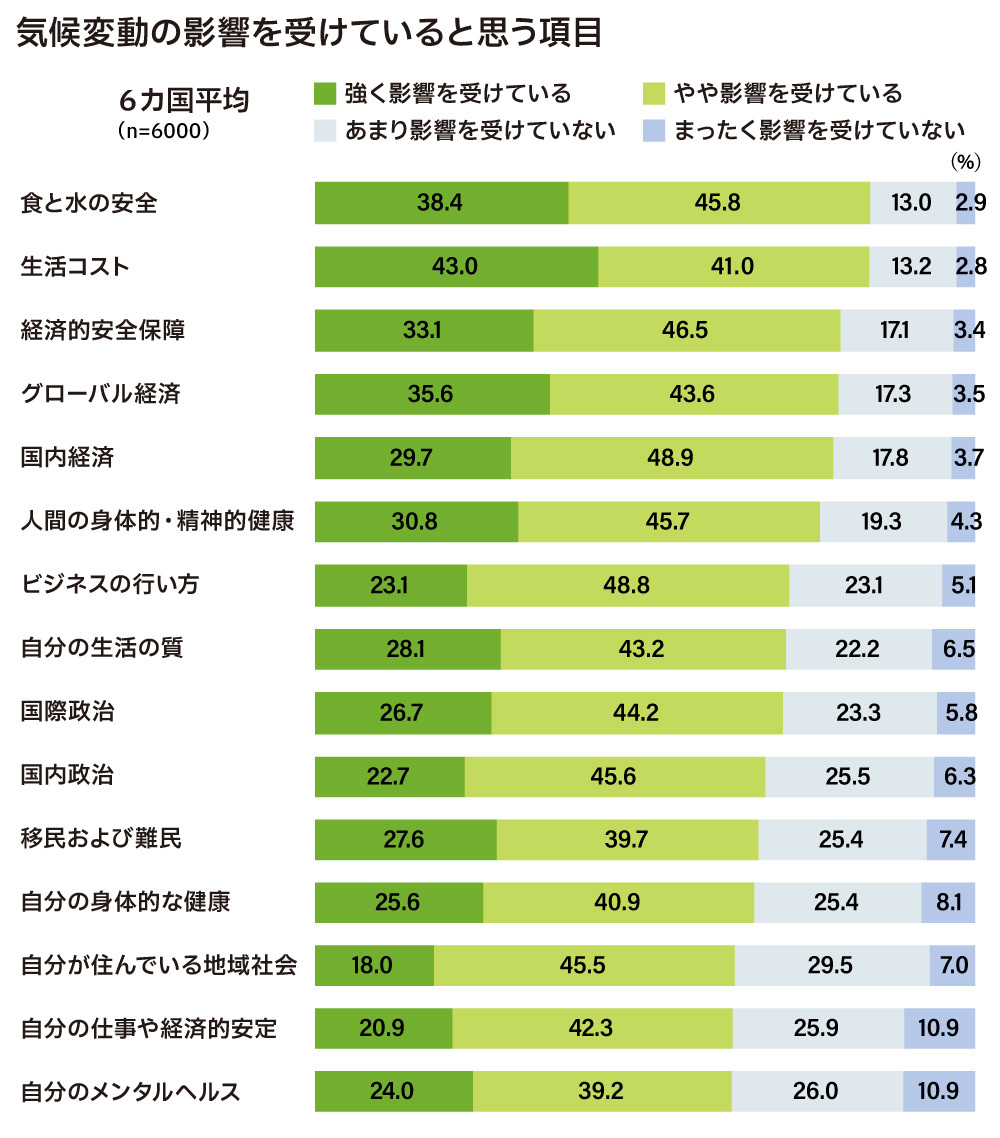

Climate change impacts "food and water" and "living costs." 2023 also brought tangible stealth price hikes

As "areas affected by climate change," over 80% of respondents across six countries cited "food and water safety" and "living costs." These items also exceeded 80% in the United States.

In Japan too, the combined proportion of those reporting "strongly/somewhat affected" exceeded the majority for all items presented. This indicates a growing awareness that climate change is no longer a future crisis but is already impacting daily life. Furthermore, economic-related items ranked highly in every country, showing that the economic impact of climate change is being felt globally.

While "my mental health" ranked lowest on average across the six countries, the results reflected the attention given in Europe and the US to "Climate Anxiety among Generation Z caused by climate change." Specifically, 65% of French Gen Z respondents (9 points above the French average) and 74% of German Gen Z respondents (10 points above the German average) selected this item.

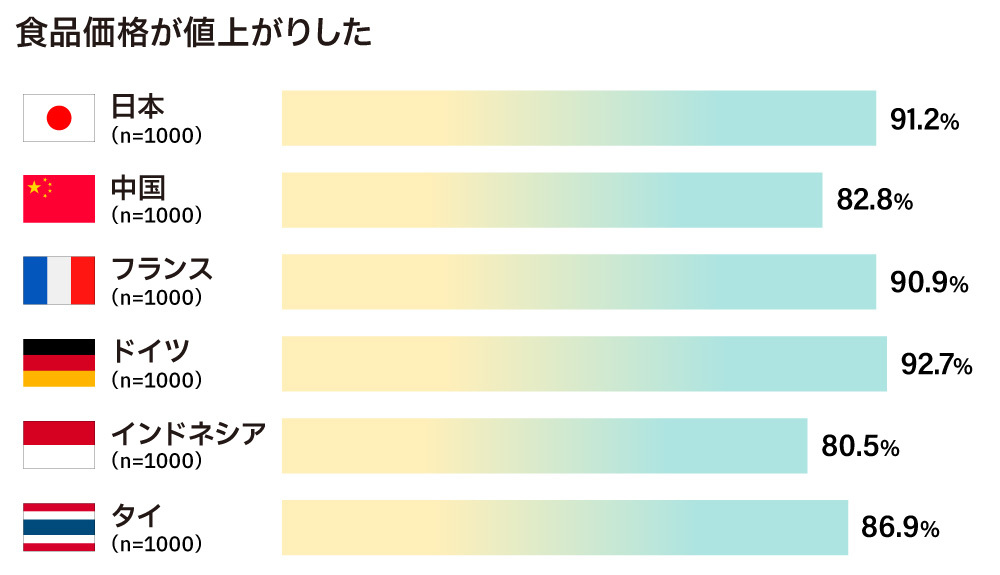

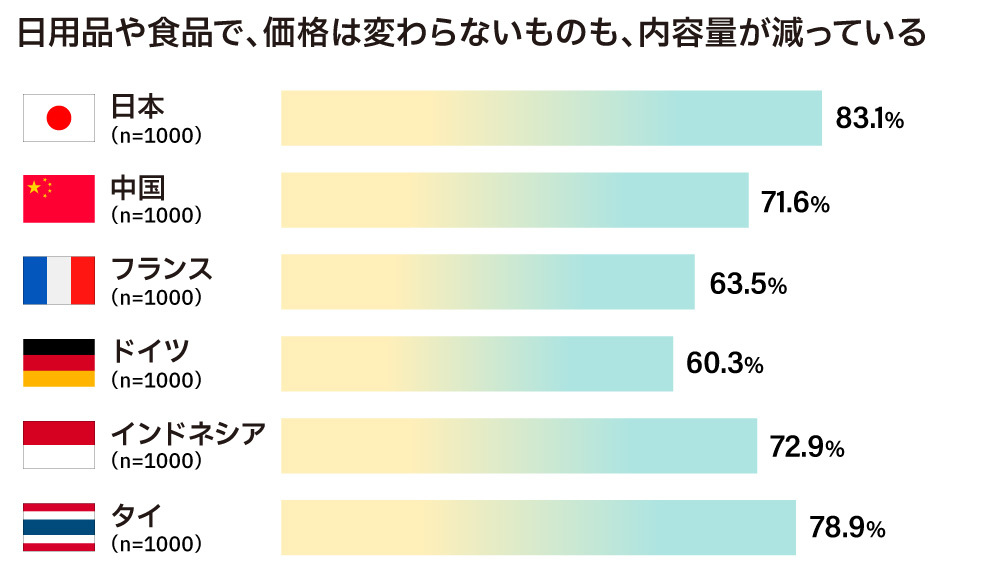

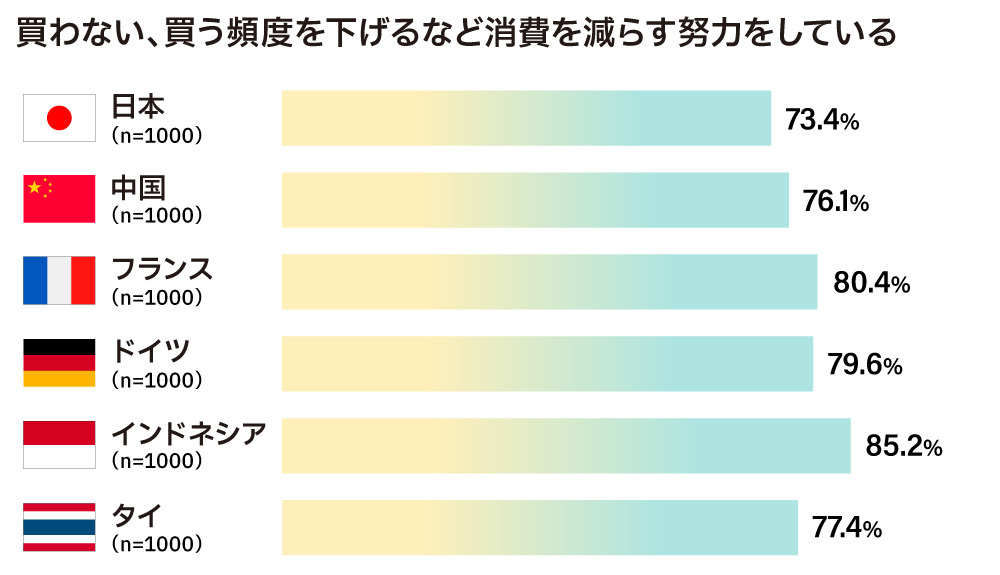

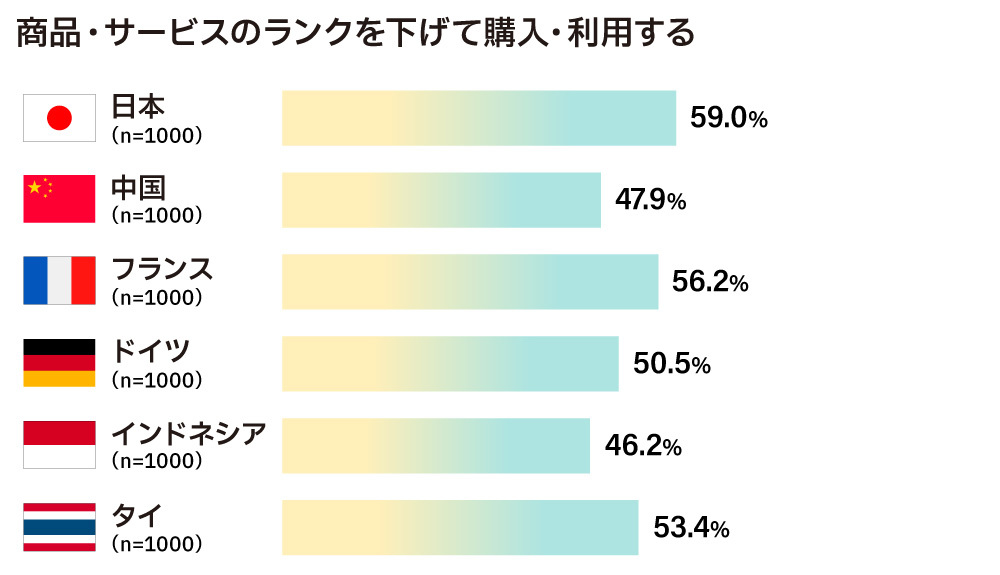

Regarding living costs, the six-country average for responses indicating prices "increased" in 2023 (combining "strongly agree" and "somewhat agree") showed 88% for "food prices," 86% for "fuel costs," and 85% for "utility bills," indicating widespread inflation concerns. Additionally, 72% of respondents across the six countries, and 83% in Japan, felt they were experiencing de facto price increases, such as reduced product quantities at the same price, also known as stealth price hikes. In Japan, 59% of respondents reported "purchasing or using lower-tier products/services," the highest proportion among the six countries.

Refill packs for daily necessities? Or container recycling?

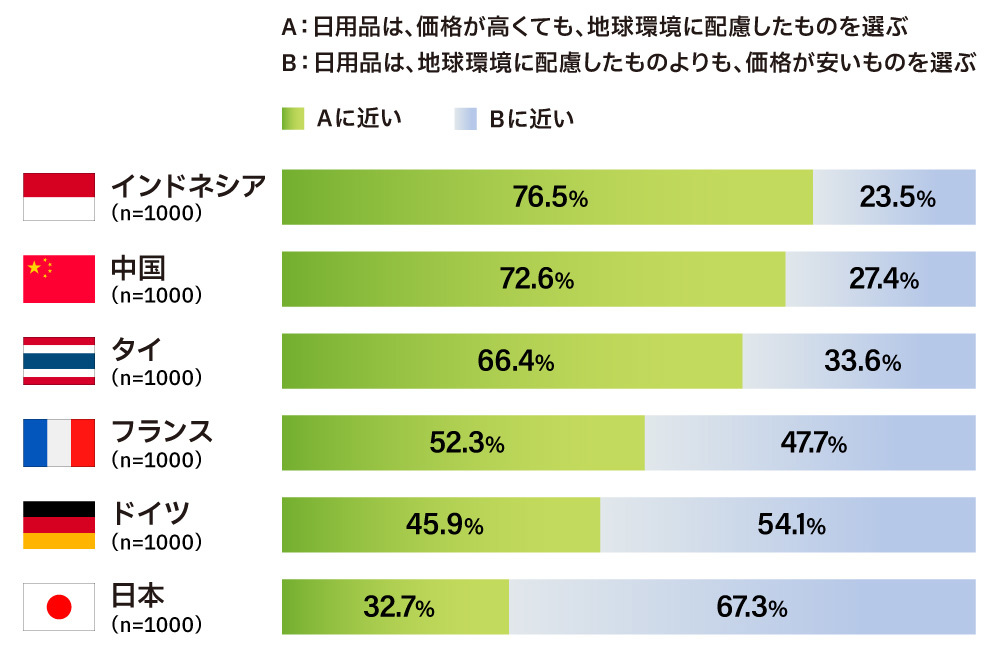

Next, we introduce items specific to daily necessities. First, regarding purchasing priorities. Since the first survey, we have asked whether respondents choose "environmentally friendly daily necessities even if they are more expensive (environment priority)" or "cheaper daily necessities over environmentally friendly ones (price priority)". In Japan, 30% chose environment priority and 70% chose price priority, while Indonesia, China, and Thailand showed the opposite, with 70% choosing environment priority. France and Germany were roughly split 50/50, and the overall trends haven't changed significantly since 2021.

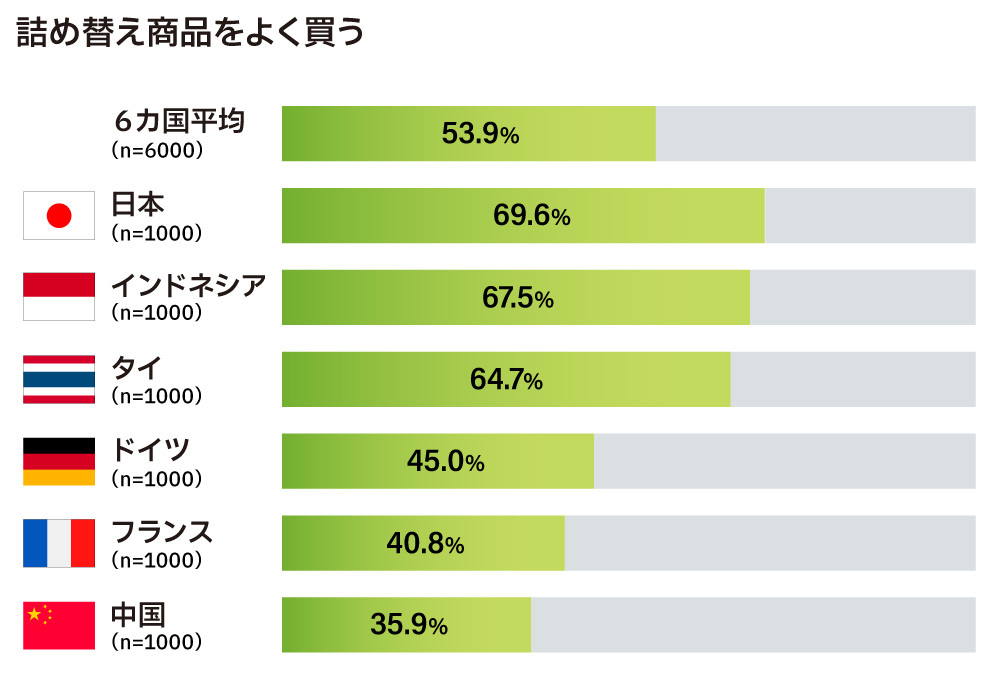

Next, regarding purchasing refill products: The percentage who answered "I often buy them" was 70% in Japan, 68% in Indonesia, and 65% in Thailand. Other countries were below half: Germany at 45%, France at 41%, and China at 36%.

For example, with shampoo, refill products are placed in the main shelf zone in Japan, Thailand, and Indonesia, while in other countries, the main bottles are primarily displayed. Additionally, in Southeast Asia, many people tend to "use the refill pack as is" without transferring the contents. In China, many people "have reservations about the refilling process" (concerned that exposure to air or residual water after washing the container could alter product quality), and the perceived barriers to refilling differ from the Japanese perspective.

Furthermore, the concept of "refill packs" isn't necessarily as widely recognized as in Japan. Higher-priced options exist, such as refill stations where customers bring their own containers for bulk purchases, services where containers brought to the store are cleaned and refilled, and home delivery services that include container collection.

Now, keeping in mind these differences in "price priority vs. environmental priority" and "how often refill products are purchased," we will examine: "If buying daily necessities priced 1.3 times higher than current products, to what extent would environmental factors contribute to premium purchasing decisions?" Incidentally, the 1.3x figure references responses indicating willingness to pay more in response to the 2021 question: "If a product launched that was both higher quality than current offerings and environmentally friendly, how much more would you be willing to pay?"

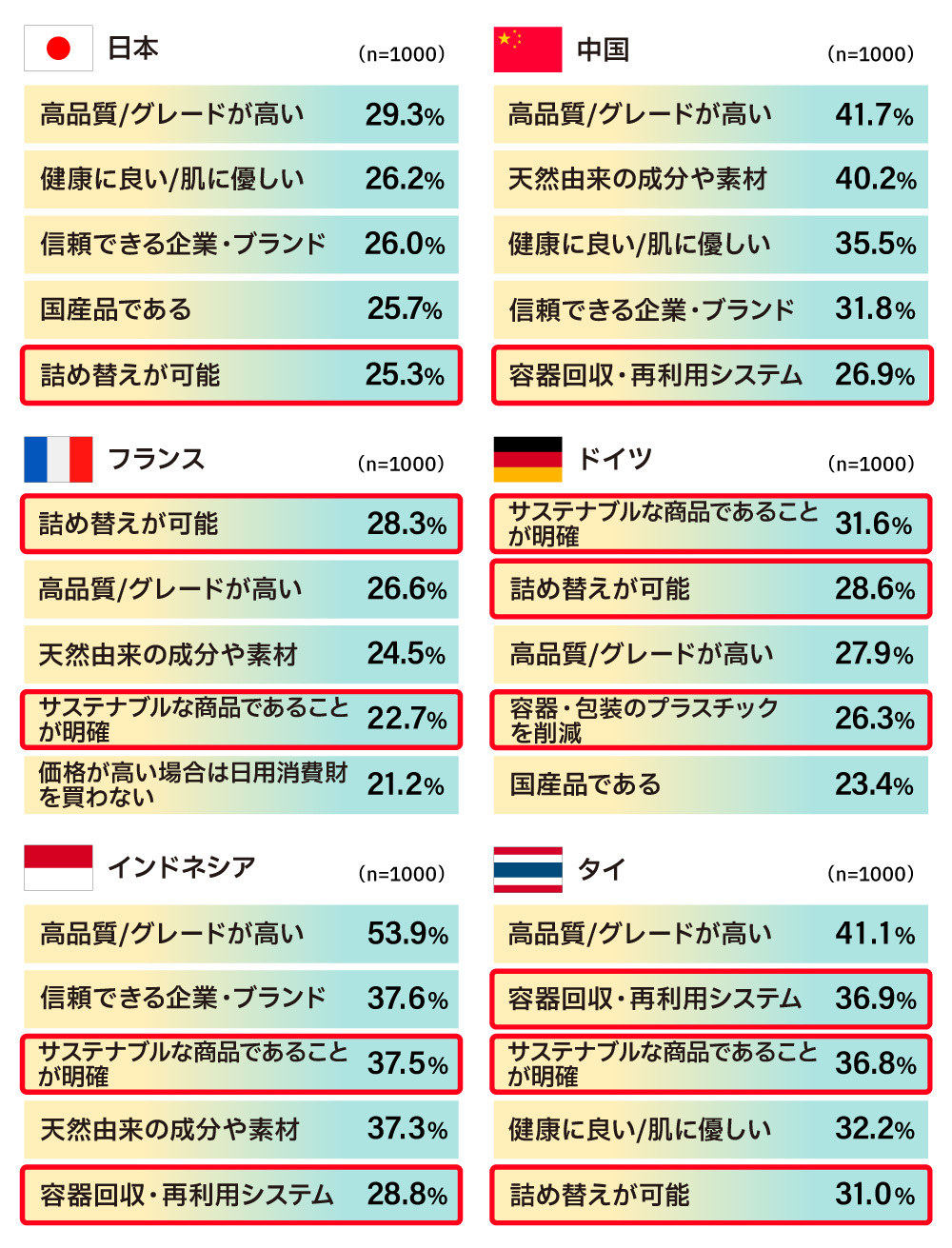

France and Germany saw environmental factors become the top premium purchase reason for daily necessities. In Asia, "high quality" is the top reason for premium purchases. Among the top five purchase reasons, container-related factors are listed below.

- Refillable packaging: Japan (25.3%), France (28.3%), Germany (28.6%), Thailand (31.0%)

- Container collection/reuse systems: China (26.9%), Indonesia (28.8%), Thailand (36.9%)

- Reduced plastic in packaging: Germany (26.3%)

While container collection and reuse are not widely considered in Japan, expectations are high in other Asian countries. Furthermore, in Germany and France where refill purchases are not yet a daily habit, it might be possible to position the product as "a premium item offering a choice of refill systems—container collection, refill, home delivery, etc." ( ).

Resistance to not eating beef is decreasing

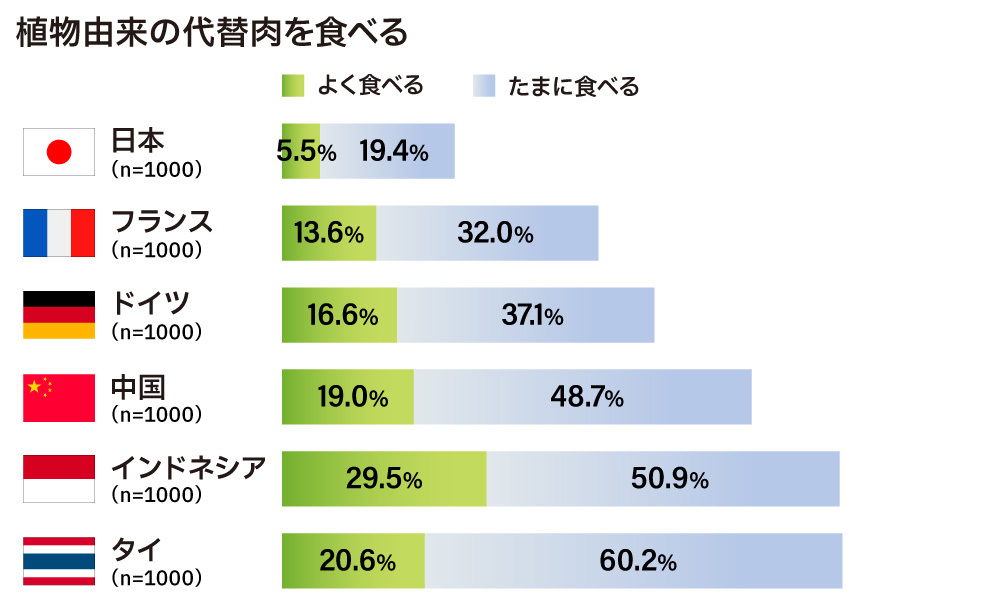

Finally, we examine the penetration and consumer intent for plant-based meat alternatives (made from soy and other plant sources), now widely available in many Japanese supermarkets.

First, while the number of people who "often eat" plant-based meat alternatives is still small, and few have made it a regular habit, including those who "occasionally eat" it suggests a certain market exists. Notably, only in France and Germany does the proportion of Generation Z eating these plant-based alternatives ("often eat" + "occasionally eat") reach 64% each, more than 10 percentage points above the national average, indicating higher acceptance among Generation Z in Europe.

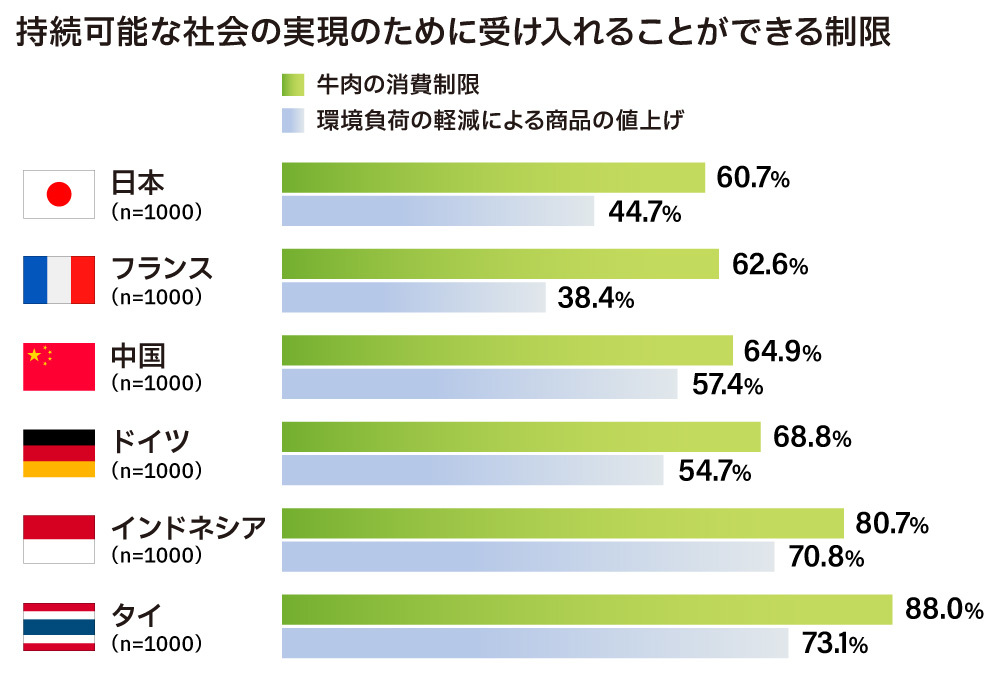

Reasons for choosing alternative meat vary, including veganism, religious reasons, dieting, climate change mitigation, and animal welfare. Among these, when asked about limiting beef consumption due to climate change impacts, over 60% in all countries accepted this restriction—a higher acceptance rate than for "price increases due to reduced environmental impact." Even in countries like France and China that value their food culture, the need to reduce beef consumption appears conceptually understood.

Restricting beef consumption doesn't necessarily lead to alternative meat consumption. Even if people understand the concept intellectually, without actual restrictions, it seems likely to take time for voluntary habits to form. In the Netherlands, beef prices rose in 2022, making alternative meat cheaper than beef. Going forward, economic factors may increasingly drive the choice of alternative meat.

As shown in the graph, "price increases due to reduced environmental impact" are acceptable to 40-50% of people in Japan, France, and Germany, and 70% in Indonesia and Thailand. Countries with limited economic growth prospects, where wages struggle to keep pace with rising prices, may find further increases in living costs psychologically difficult to accept.

The ideal scenario is not a choice between abstaining from purchase or accepting higher prices for environmental benefits, but rather selecting products one genuinely likes that "happen to be sustainable." However, against a backdrop of inflation and economic downturn, a mindset prioritizing price over environmental concerns remains deeply entrenched. Faced with the reality that neither people nor companies move significantly based on ideals alone, both seem to be beginning to accept rules and restrictions.

We plan to introduce other noteworthy topics in the future, such as social issues of interest and Generation Z and sustainability. The SLS2023 report will also be published on the DENTSU SOKEN INC. website.

[Survey Overview]

Target Areas: 6 countries (Japan, China, France, Germany, Indonesia, Thailand)

Respondent Criteria: Ages 18–69 (Gender response options: "Male," "Female," "Other/Prefer not to answer")

Sample Size: 6,000 respondents (1,000 per country)

Survey Method: Online survey

Survey Period: July 12 to August 21, 2023

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Back Numbers

Author

Rie Tanaka

株式会社電通ライブ

シニアディレクター

After working at a telecommunications company, he joined Dentsu Inc. Following the establishment of insight research teams such as Dentsu Wakamon and the Food Lifestyle Lab, he was seconded to Dentsu Digital Inc. in 2016 and to the Data Science Department of a consumer goods manufacturer in 2017, where he worked on digital transformation (DX).In 2019, he returned to the Dentsu Global Business Center. After holding concurrent roles within the Dentsu Group, he has led international research, branding, and consulting at the Sustainability Consulting Office since 2023. Since 2022, he has served as Executive Coordinator at the Kanazawa University Organization for the Promotion of Advanced Science and Social Co-creation. Since 2024, he has been a partner at the certified NPO Service Grant. He will be seconded to Dentsu Live Inc. starting in 2026.

![[SB 2026 Tokyo] What Is Required of Corporate Sustainability Communicationsのサムネイル](https://cdn.speedsize.com/e7df76a9-4406-40f5-bc97-57e7c2c2d99d/https://cdn.dentsu-ho.com/834def09-4013-422a-a14f-45c659fd7b82/gbc33_top.jpg/f_auto,w_3840)