Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

Gang of Four: U.S. Advanced ICT Companies Entering the Financial Markets

Mototsune Sato

NCB Lab.

Yoshitomi Sairyo

Dentsu Inc.

World-leading ICT (Information and Communications Technology) companies are leveraging cutting-edge technology to create new financial services one after another.

Google, Apple, Facebook, and Amazon.

Eric Schmidt, chairman of Google's holding company Alphabet, calls these four advanced ICT companies the "Gang of Four," saying they dominate global technology.

Led by this "Gang of Four," players in the distribution and retail and telecommunications and IT industries are easily overcoming industry barriers and entering the financial business.

In Japan, too, the "financialization of non-financial players" is gradually progressing, mainly among telecommunications carriers and distribution and retail companies.

To learn about the latest trends in the entry of companies from other industries into the financial market, Dentsu Inc. Business Creation Center's Financial Project member, Sairyo Yoshitomi, spoke with Motonori Sato, representative of NCB Lab.

Expanding Financial Businesses Using Advanced ICT Companies' Technologies

Q1. In recent years, new financial services leveraging ICT have been emerging, particularly in the US. How do you view this?

A1. While fintech startups are continuously emerging in the U.S., traditional financial institutions don't truly perceive these startups as the main threat. Instead, they view the "Gang of Four"—Google, Apple, Facebook, and Amazon—as the real challenge. These four companies possess a global customer base and cutting-edge technology. Leveraging these assets, they can provide unprecedented financial services. In fact, their ambition to enter the financial business is quite strong.

Q2. What financial services is each of the "Gang of Four" offering?

A2: Google offers Google Wallet and Android Pay. Apple provides Apple Pay. Facebook operates Facebook Credits and Messenger Pay. Amazon delivers financial services like Amazon Pay, Amazon Lending, and IoT Payments.

Google launched its mobile payment service, Google Wallet, in 2011. This sent shockwaves through financial institutions worldwide. Initially, Google Wallet was a proprietary Google service, fueling fears that it would encroach on traditional financial institutions' payment domains. By linking search logs with actual sales data, consumer behavior becomes clear, enabling personalized recommendations for various products and services beyond finance. This power is formidable.

Currently, Google has shifted its focus: it has limited its proprietary Wallet service to money transfers and transformed it into Android Pay, an open service where financial institutions can freely participate. In other words, for financial institutions, Google is no longer a threat but a potential partner. However, in terms of innovating financial services, Google still holds significant influence.

Apple

Determined not to lose to the Google camp, Apple launched its mobile payment service, Apple Pay, in 2014. This had even greater impact than Google Wallet. From the outset, it partnered with card companies and started as an open platform. Google followed suit, shifting its focus from Google Wallet to Android Pay and transitioning to an open platform. Apple Pay created the naming trend of "mobile payments are [service name] Pay."

Apple Pay arrived in Japan in October 2016. As of late May 2017, it operates in 16 countries and regions worldwide, including the US, UK, China, and Russia. Going forward, all Apple products will likely come equipped with Apple Pay. When that happens, Apple Pay will become the standard for iOS* payments, and the brands of card companies and banks will fade into the background behind Apple Pay.

※iOS

: A mobile operating system developed and provided by Apple

Social games were instrumental in Facebook's early growth. Game companies provided their own payment methods, but Facebook saw this as problematic. Since they were using Facebook's platform, Facebook insisted they should use a unified currency. Consequently, Facebook made its proprietary currency, Facebook Credits, the only option. This led to the establishment of Facebook Payments in 2011.

Before its IPO, Facebook commented that advertising revenue and payment processing revenue would be its two main pillars. However, the ratio of payments and other services to total revenue peaked at 15.9% in 2012 and has since declined, reaching 2.7% in 2016. Growing payments into a profitable business is difficult. Nevertheless, Facebook continues to pursue challenges like money transfers using the Messenger platform.

Amazon

Amazon, operator of the world's largest online marketplace, offers diverse services including payments, merchant financing, and IoT payments. Its 1-Click payment system eliminates the need to re-enter card details or shipping addresses, a convenience enjoyed by us in Japan as well.

※Merchant

: A store or business that accepts a payment service

What sets Amazon apart from the other three companies is its lending service (Amazon Lending). Its unique feature is the screening method. Lending is based not only on sales volume and the length of time a merchant has been selling on Amazon, but also on a "Customer Satisfaction Index" calculated from metrics like "Prime Order Rate," "Pre-Shipment Cancellation Rate," and "Shipment Delay Rate." This is a service for Amazon merchants; it is not available for voluntary application. Amazon invites companies with excellent sales performance to borrow through an invitation-only system.

Notable Amazon Financial Services

Q3. So, what is the most noteworthy aspect of these four companies?

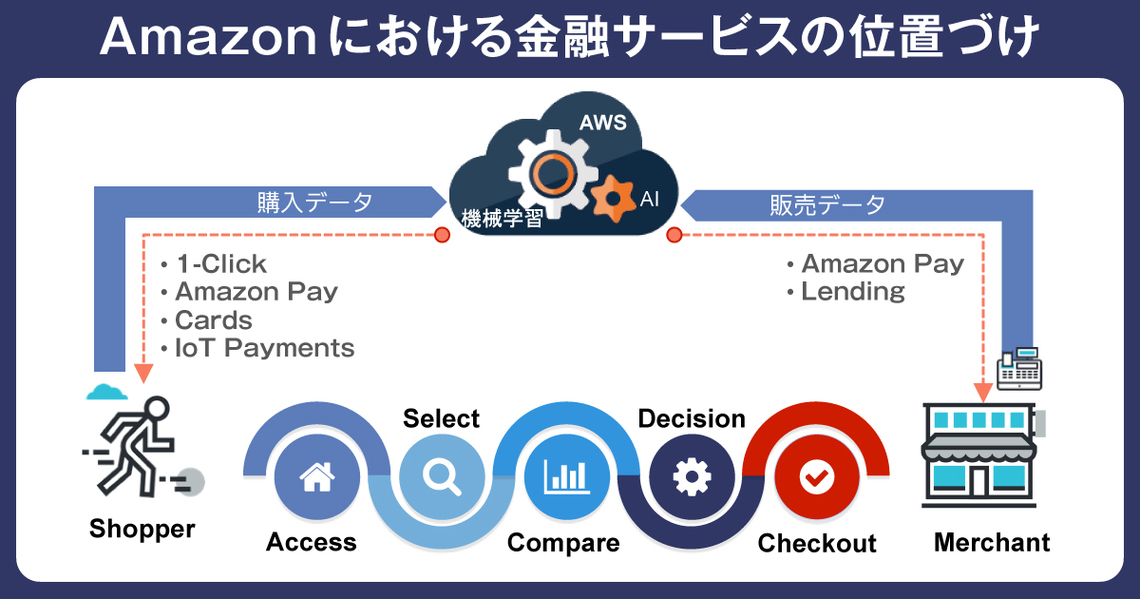

A 3: Amazon. Amazon is not only a threat to competitors in distribution and retail but is also becoming the greatest threat to traditional financial institutions. Operating a massive marketplace, Amazon possesses both user purchase data and merchant sales data. This is its strength.

Customer purchase details: "Who" bought "what" from "which merchant," "when," and "for how much." Sales data: "Which merchant" sold "what" to "who," "when," and "for how much." Leveraging both these transaction data streams, Amazon developed its merchant financing service, Amazon Lending.

What's noteworthy is its powerful drive to transform the shopping value chain. Consumers access (Access) stores, select (Select) products, compare (Compare) them with others, make a decision (Decision), and then purchase (Checkout). Amazon is relentlessly eliminating friction points like hassle and stress within this value chain to enhance customer experience value. Traditional financial institutions and fintech ventures often lack this perspective, frequently focusing solely on profit generation. Amazon aims to deliver unprecedented CX (Customer Experience).

Q4. Are there examples of new CX offerings brought about by Amazon's shopping value chain transformation?

A4: While still in the experimental phase, Amazon Go is a prime example. They developed a cashierless store utilizing cutting-edge technology. Customers launch the app upon entering, scan a QR code to pass through the gate. The gate functions like a train ticket barrier. As they pass through, cameras perform facial recognition, verifying the individual using both the QR code and facial data.

Customers simply select items inside and exit through the gate. Sensors determine what was purchased. Upon exiting, the purchase amount is charged to the customer's Amazon account, and a receipt is automatically sent. There is no need to wait in line at a register or go through checkout.

This service delivers an unprecedented shopping experience: enter through the gate, select and pick up items, exit the gate, and your shopping is complete. Amazon's internet-connected cloud (AWS) powers this service. Sensors capture every aspect of the customer's in-store behavior: their path through the store, which shelves they stopped at, which items they picked up, whether they placed them in their shopping bag or returned them to the shelf, and what other items they purchased alongside them. All this data is uploaded to the cloud. In the cloud, AI and machine learning* process this data into precise purchase information: "Who bought what, when, and for how much." A receipt is sent, and the amount is debited. This is IoT payment. Traditional financial institutions would likely never conceive of such an approach.

※Machine Learning

: The process of using artificial intelligence to analyze data and identify unique patterns

Q5.What is the core competency of Amazon's business model?

A5: I believe there are three.

① Customer Obsession

② Expansion of an outward-facing economic sphere through open alliances

③ Superior Technology

① Customer Obsession

This philosophy goes a step further than customer-centric or customer-first approaches. It's not just the superficial notion that "the customer is always right." For example, the Amazon Dash Button service was born from the problem of how to make purchasing everyday items like detergent and toilet paper easier and more convenient.

By placing an Amazon Dash Button next to the washing machine, customers can order detergent with a single press when they notice it's running low. This eliminates the hassle of accessing the Amazon marketplace, searching for the product, placing an order, and completing payment. It was precisely this obsession with the customer that enabled the development of such a service.

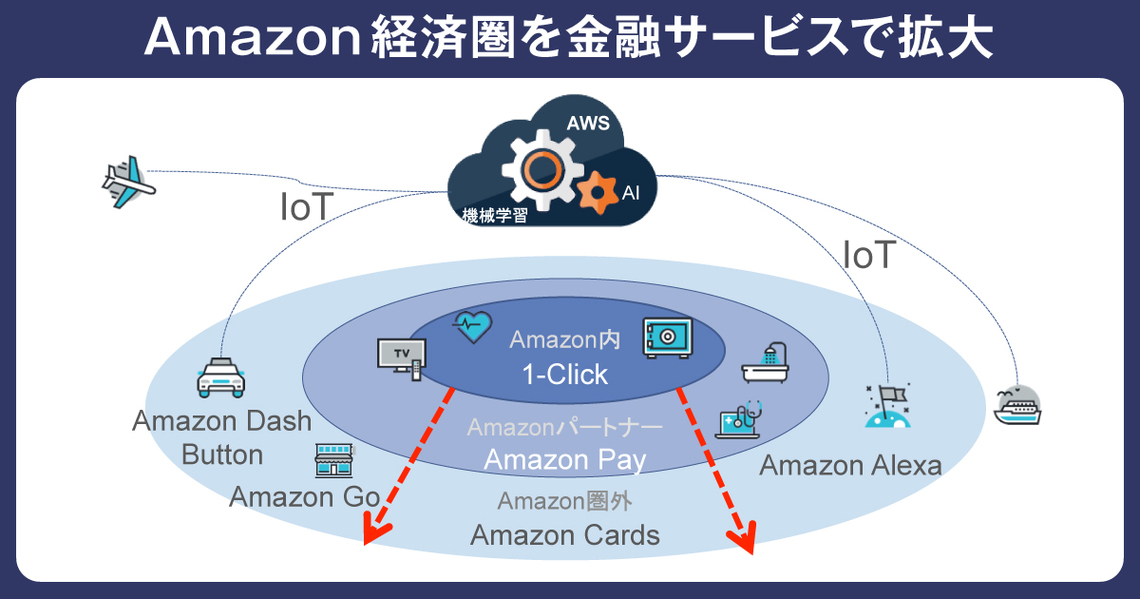

② Expanding the Outward-Facing Economy Through Open Alliances

This is clearly evident in payment services. Amazon Marketplace uses 1-Click payment. Amazon Pay extends this same mechanism as an open platform available to other businesses. For merchants outside this ecosystem, there's the Amazon Card (credit card) featuring international brands. Furthermore, Amazon is now aiming to spread IoT payments across all domains by leveraging Amazon Go and Amazon Dash Button. Consequently, it can be said that Amazon is actively expanding its economic sphere outward.

③ Superior Technology

This includes cloud services (AWS), AI, machine learning, and sensing technologies. Voice recognition and response technology is also outstanding. Alexa, a virtual assistant* utilizing this voice recognition and response technology, is rapidly expanding into households across the United States.

*Virtual Assistant

: A system that uses AI to provide users with advice on features they may not notice, delivered via text or voice.

While Amazon is strongly associated with commerce, its technology is at the global forefront. It's typical of Amazon to generously open these technologies to the public as an open platform. By doing so, it aims to expand its economic sphere and accelerate technological evolution. For traditional financial institutions, Amazon is a formidable presence.

The Arrival of the Great Competition Era for E-Commerce and Career Economic Spheres in Japan

Q6.In Japan too, especially telecom carriers and distribution/retail companies are expanding into financial services. How do you view this?

A6: They certainly pose a threat to Japan's traditional financial institutions. Telecom carriers are positioned closest to their customers. They are entities deeply integrated into people's daily lives. Every telecom carrier positions lifestyle support businesses—combining financial services like card operations, remittance services, and insurance—as future growth areas and is investing heavily in them.

The strength of retail and distribution companies lies in their marketplace customer touchpoints. Aeon Group's financial services now lead all other business segments in operating profit, accounting for 33% of the total. Seven & i Holdings' financial-related businesses contribute 13% of operating profit, making them the second-largest profit driver after convenience stores.

Rakuten bundles its financial services—Rakuten Card, Rakuten Bank, Rakuten Life Insurance, Rakuten Securities—under its fintech business. Fintech has grown to account for 54% of operating profit. One could now view the Rakuten Group not as a commerce sector player, but as a financial group.

For traditional financial institutions, companies with marketplaces must be enviable. They have a large base of users and merchants. They can provide financial services to both.

Q7.Competition is intensifying as non-financial industries enter the financial services market. What will be required of financial services going forward?

A7: Amazon's core competencies, mentioned earlier, will likely serve as a benchmark. I believe three things are essential: "Customer Obsession," "Open Alliances," and "Superior Technology."

No customers, no profits. Solve inconveniences from the customer's perspective. Transform processes into more convenient ones based on customer behavior. Empathize with customers to deliver more comfortable experiences. That's the mindset we need. Customers won't engage with businesses that merely copy Western fintech models.

In this era of hyper-speed digitalization, it's becoming increasingly difficult for a single company to handle everything. It's crucial to adopt an open financial platform approach, collaborating with specialized partners in each domain to drive business forward.

Regarding the latest technology, I recommend using services like Amazon or Google as your foundation. They offer cloud-based AI, machine learning, and voice recognition/response software. And they're cost-effective. The focus should be on mastering technology, not competing on technology itself.

In other words, the most crucial of these three is "Customer Obsession." Businesses that earn and maintain customer support will inevitably succeed. I hope you'll take this philosophy as a model and challenge yourselves to innovate financial services.

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Author

Mototsune Sato

NCB Lab.

Representative

Born in 1952. Founded ISI, a specialized consulting firm for cards and payments, in 1989. Appointed as head of the Japan Card Business Research Institute (now NCB Lab.) in 1997, aiming to promote and develop card payments. Author of numerous books including 'Electronic Money Wars', 'New Credit Business', 'Digital Word Power', 'Card & Credit Terminology Dictionary', 'New Payment Report', and 'Fintech Report'. His accessible explanations are well-received, and he is also active as a lecturer and moderator.

Yoshitomi Sairyo

Dentsu Inc.

BX Creative Center, Experience Design Department

Senior Planning Director

Head of the Dentsu Cashless Project. Joined Dentsu Inc. after working at a U.S.-based consulting firm and a European investment bank. Engaged in new business development, marketing and brand strategy, and PR for clients in finance (banks, securities, insurance, etc.), telecommunications, automotive, beverages, toiletries, and pharmaceuticals. Contributions include "Corporate Reputation" (Advertising) and "CSR and Corporate Reputation" (Nikkei Branding). Certified Member of the Securities Analysts Association of Japan.