Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

Can Mobile Payments Break Down the Barriers to Cashless Adoption for Small and Medium-Sized Stores?

Dentsu Inc. conducted its 7th "Consumer Cashless Awareness Survey" in December 2024. This edition focused on clarifying the actual usage patterns of mobile payments.

"Could structural changes be emerging in Japan's cashless payments?"

Based on this hypothesis, Last time focused on the latest trends among cashless users.

This time, we focus on the trends among small and medium-sized businesses introducing cashless payments,

- Is cashless usage progressing at stores that accept cashless payments?

• How interested are cashless payment accepting stores in mobile payments?

We will examine survey results addressing these questions.

How is the major turning point in Japan's cashless payments, driven by cards, impacting stores? Following Part 1, Dentsu Inc.'s Saio Yoshitomi will provide an overview of Japan's current cashless payment landscape.

<Table of Contents>

The "Spring" of Cashless Adoption for Small and Medium-Sized Stores Remains Distant

Mobile QR payments now account for about 80% of adopted payment methods, closing in on card payments

Mobile QR payments are key to increasing the number of stores adopting cashless

Also Watch for Rising Adoption Rates of Mobile Contactless Payments Like Apple Pay and Google Pay

Cashless payments drive the advancement of financial services

The "spring" of cashless adoption for small and medium-sized stores remains distant

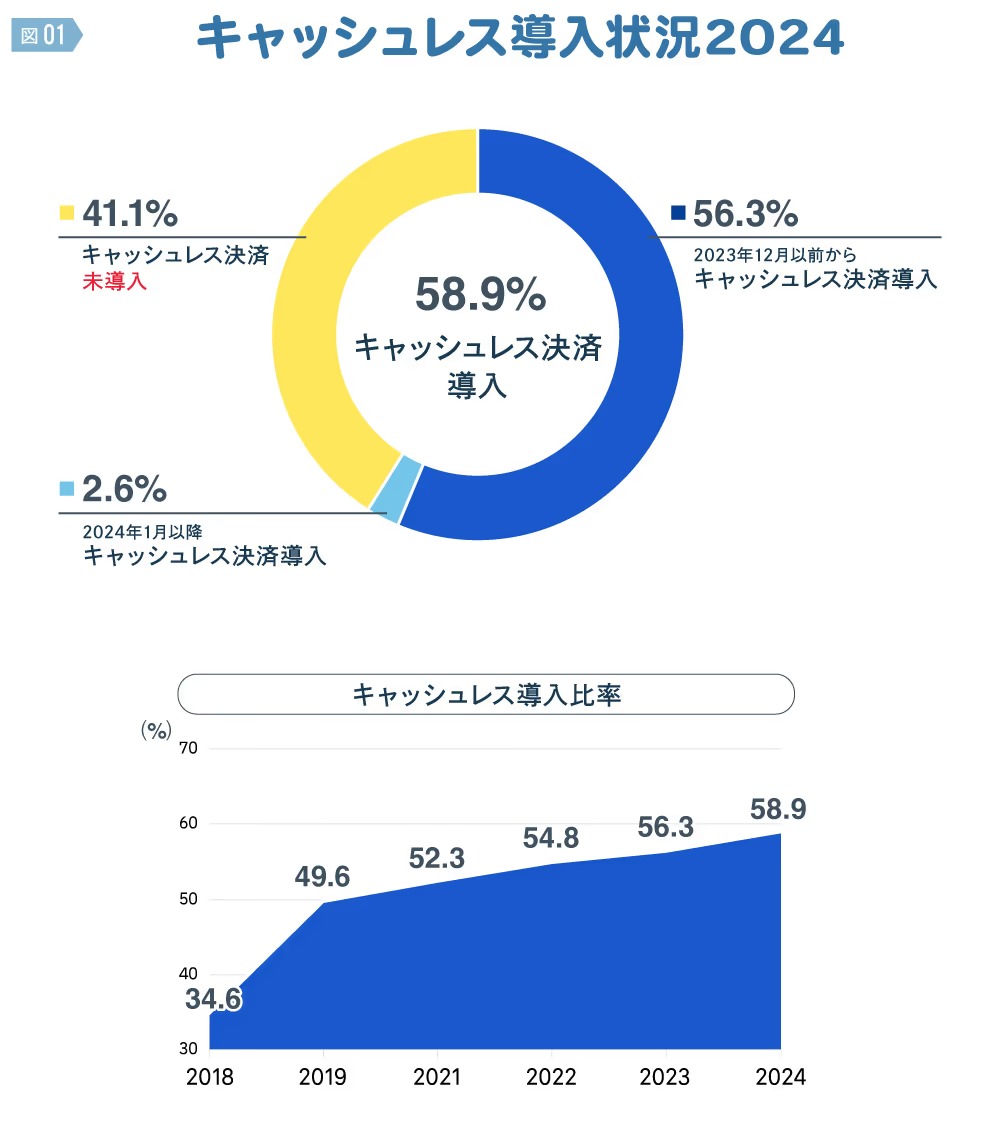

Based on the 7th survey conducted in December 2024, we examine the cashless payment adoption status among small and medium-sized businesses (merchants).

First, what is the latest status of cashless payment adoption among small and medium-sized businesses?

Only 2.6% of merchants introduced cashless payments since January 2024. Cashless adoption among small and medium-sized businesses is progressing only gradually. Including these new adopters, the cashless payment adoption rate stands at 58.9%. Growth has slowed since the start of 2024.

Rising prices are inflating procurement costs, yet businesses cannot pass these increases on to sales prices, leading to tight cash flow. Paying transaction fees for adoption seems unthinkable. You can almost hear these voices. To break through the 41.1% barrier of non-adoption, a significant driving force is required. Mobile payments could potentially become that catalyst.

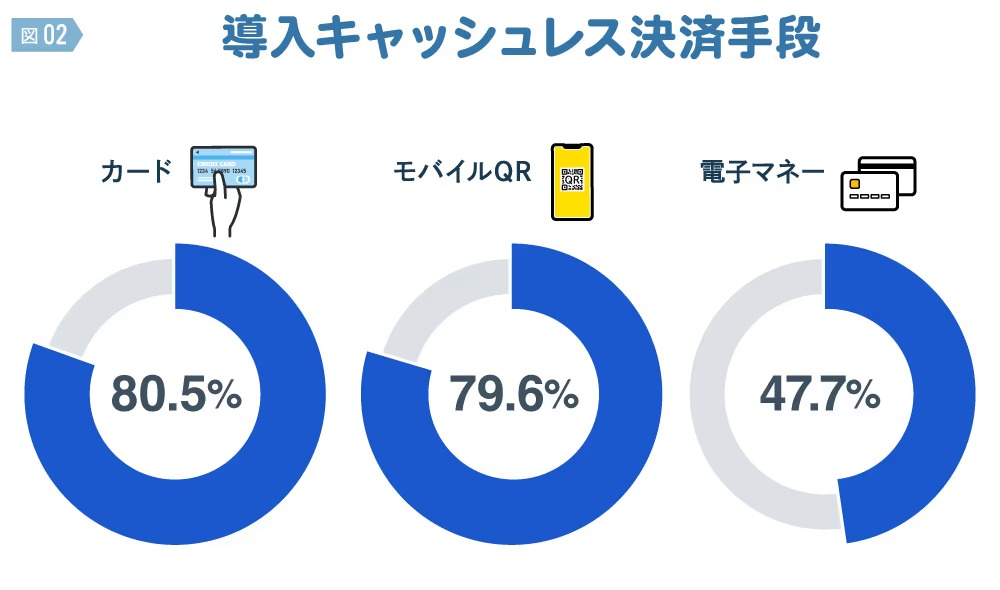

Among adopted payment methods, "mobile QR payments" reached about 80%, closing in on card payments.

What payment methods are cashless-enabled stores adopting? Initially, "cashless acceptance" primarily meant card acceptance. That landscape is changing significantly.

In this survey, while cards remained top at 80.5%, mobile QR payments followed closely in second place at 79.6%. The gap was a mere 0.9 percentage points. Just over five years after mobile QR payments truly took off, they have caught up to and are now spreading with such momentum that they could soon overtake cards.

Electronic money systems introduced in the 2000s, including "transportation cards (Suica, PASMO, etc.)" and "retail cards (WAON, nanaco, etc.)," have finally reached just under 50% (47.7%) after about 20 years. The difference in payment acceptance terminals appears to be the gap between these established systems and the emerging force of mobile QR payments. Like cards, e-money requires high-spec payment terminals, leading to higher initial costs and transaction fees. Mobile QR payments, however, can be accepted with simple QR code stickers or POP displays, making them attractive due to low initial costs and lower transaction fees.

This survey also found that among cashless-enabled stores, 18.5% accept mobile QR payments but not cards. The key to increasing the number of cashless-enabled stores lies in mobile QR payments.

Mobile QR payments are key to increasing cashless adoption

Which industries are leading the adoption of cashless payments?

This survey found convenience stores have the highest adoption rate at "100%". Convenience stores, which many consumers visit casually, offer a wide range of cashless payment options to enhance convenience.

The next most advanced sector is clothing stores (73.7%). While not shown in the graph, mobile QR payment adoption within this category was 74.8%. Bars and liquor stores came in a close third (72.7%), with mobile QR payment adoption at 71.3%. This indicates mobile QR payments are also gaining traction in these sectors, which typically have higher average customer spending.

Fast food ranks fourth. While the overall adoption rate of 66.7% is not exceptionally high, looking at payment methods specifically, the adoption rate for mobile QR payments was 100%.

While the overall cashless adoption rate is low, some sectors predominantly use mobile QR payments. These include fresh food and liquor sales, and coffee shops. This situation is perhaps easiest to visualize by imagining payment scenes at neighborhood shopping district greengrocers, fishmongers, liquor stores, and coffee shops.

While the cashless adoption rate for fresh food is only 22.9%, 87.5% of the payment methods adopted there are mobile QR payments. For liquor sales, 36.7% accept cashless payments, and 94.1% of those use mobile QR payments. The cashless adoption rate for coffee shops is 42.9%, and 95.8% of those have adopted mobile QR payments.

The fact that mobile QR payments are consistently adopted even in industries with low cashless adoption rates clearly indicates that they are leading the charge in capturing the 41.1% of small and medium-sized businesses that have yet to adopt cashless payments. It is undoubtedly mobile QR payments that are driving the adoption of mobile contactless payments, such as Apple Pay and Google Pay, which are also seeing increased adoption rates

Attention is also turning to the increasing adoption rate of mobile contactless payments like Apple Pay and Google Pay.

When asked if mobile payment usage had increased in the last three months, 36.5% of cashless-enabled stores answered "increased." The breakdown was 5.1% "increased significantly" and 31.4% "increased somewhat."

Breaking down mobile payments into mobile QR payments (PayPay, d-barai, etc.) and mobile contactless payments (Apple Pay, Google Pay, etc.), 35.2% reported an increase for mobile QR payments, while 28.9% reported an increase for mobile contactless payments. This appears to align with the trend of increased mobile payment usage among consumers. Even among small and medium-sized stores, mobile contactless payments are growing alongside mobile QR payments.

Mobile contactless payments are likely to increase further. Driving this growth is the "iPhone Touch Payments" service launched in May 2024. This allows smartphones owned by small and medium-sized stores to function directly as contactless payment terminals, eliminating the need to install expensive dedicated contactless payment terminals. This functionality is already available on Android devices. Incidentally, the smartphone ownership rate among small and medium-sized store owners is 93%. The breakdown shows 49.2% use Android devices and 43.8% use iPhones.

When asked whether they would use their existing smartphone as a contactless payment terminal, responses combining "Definitely want to use it" (5.8%) and "Somewhat want to use it" (19.3%) totaled 25.1%.

This includes responses from stores not yet adopting cashless payments, indicating that one in four stores has a positive attitude toward introducing mobile contactless payments. However, the main factor preventing adoption is the issue of fees. Indeed, in this survey, 57.2% of stores not yet using cashless payments cited high fees as the reason. 57.2% of stores not yet using cashless payment cited high fees as a reason.

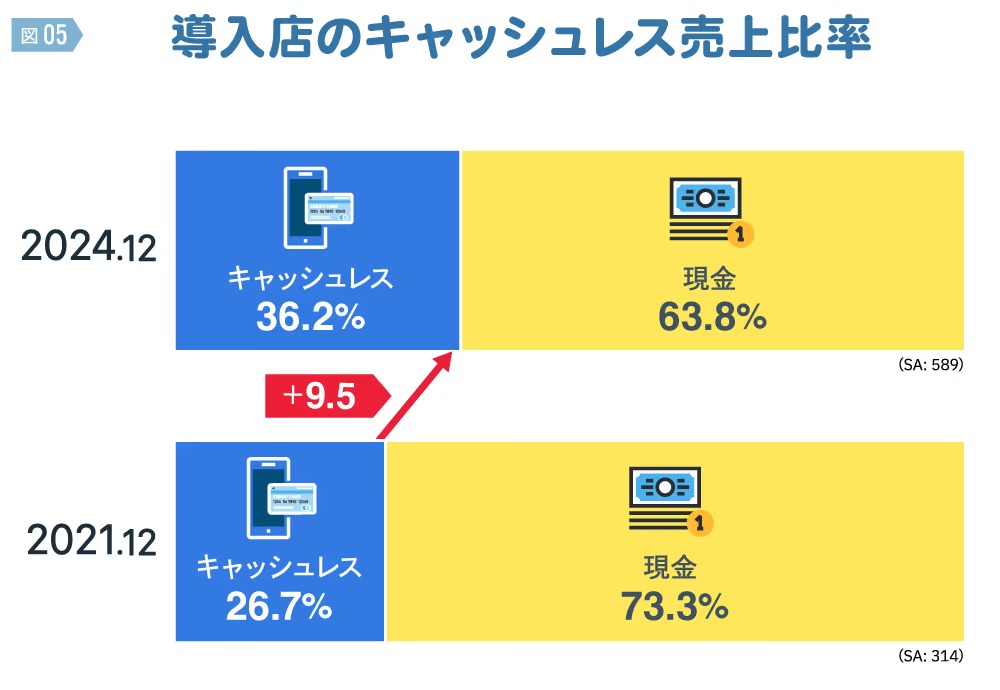

The harsh reality: cashless sales ratio is a mere "36.2%"

We asked merchants about the recent cashless sales ratio as a percentage of their total sales. The December 2024 survey showed an industry-wide average of 36.2%, an increase of 9.5 percentage points since December 2021. However, the cash ratio remains high at 63.8%.

The cashless sales ratio was higher than average for convenience stores (47.3%) and clothing retailers (41.4%). This trend has remained unchanged since 2021.

Furthermore, 24.1% of small and medium-sized stores had a cashless sales ratio exceeding 50%, meaning one in four cashless-enabled stores prioritizes cashless over cash. A small but notable 1.4% of small and medium-sized stores were 100% cashless.

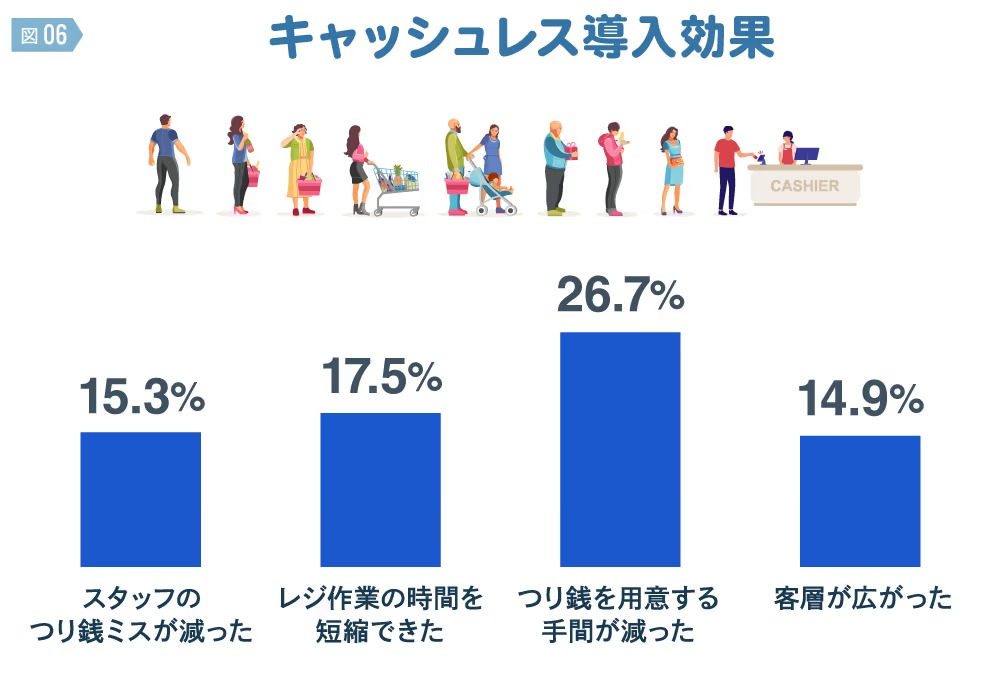

When asked about the benefits of adopting cashless payments, the top response was "Reduced the hassle of preparing change" (26.7%). This was followed by "Shortened checkout time" (17.5%) and "Reduced staff errors with change" (15.3%). All these represent operational improvements. The higher the cashless ratio in sales, the greater the tendency for these benefits to be felt.

Cashless systems also offer marketing benefits. 14.9% of small and medium-sized businesses reported "a broader customer base." Responses included "attracting foreign tourists" (5.3%) and "enabling management of customer and sales data" (5.3%). Some also noted "increased sales due to cashless" (8.8%). To promote cashless adoption, it is crucial to patiently communicate its benefits to small and medium-sized businesses The voices of small and medium-sized stores achieving results are persuasive.

Cashless payments are driving the advancement of financial services

A structural shift is evident in this survey: cashless payment methods are transitioning from cards to mobile.

Mobile payments (42.8%) became the most frequently used cashless payment method among consumers, significantly outpacing cards (33.0%). This result indicates mobile payments have become the primary cashless payment method.

Furthermore, the shift from cards to mobile as the payment tool has made financial services more accessible than ever before (For details, see Part 1 ).

Mobile payments function like using a digital wallet directly for transactions, replacing the physical wallet. Unlike a physical wallet with limited capacity, a digital wallet can be linked to financial services like investments and insurance that previously couldn't fit in a wallet.

Moreover, using mobile payments often earns you points. You can instantly view the points earned from payments and redirect them toward investments or insurance. Funds increased through investments can then be used for purchases, creating a cycle where payments and financial services integrate and funds circulate.

Japan's cashless movement has transcended mere payment functionality, driving the advanced evolution of financial services. Mobile payments possess the power to integrate and fuse diverse content, thereby advancing DX within consumers' daily lives.

For small and medium-sized stores, mobile QR payments may finally mark the beginning of their digital transformation. The cashless adoption rate stands at 58.9%. While 40% still haven't adopted cashless, among those that have, mobile QR payment acceptance (79.6%) is closing in on card acceptance (80.5%) (Figure 02).

Mobile payments have the potential to break down barriers to cashless adoption for small and medium-sized stores. Dentsu Inc. Cashless Project will continue investigating Japan's cashless landscape and closely monitoring these trends.

[Survey Overview]

7th Survey on Cashless Awareness Among Consumers

・Purpose: To understand changes in consumers' payment methods

・Target Area: Nationwide

・Respondent Criteria: Men and women aged 20–69

・Sample Size: 1,000 ※

・Survey Method: Online survey

・Survey Period: December 1, 2024 - December 3, 2024

・Survey Agency: Rakuten Insight Inc.

* The 1,000 respondents were weighted to match the sex and age distribution of the population (based on the 2022 National Census). "%" and "n" represent the weighted scores and sample sizes, respectively.

The information published at this time is as follows.

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Author

Yoshitomi Sairyo

Dentsu Inc.

BX Creative Center, Experience Design Department

Senior Planning Director

Head of the Dentsu Cashless Project. Joined Dentsu Inc. after working at a U.S.-based consulting firm and a European investment bank. Engaged in new business development, marketing and brand strategy, and PR for clients in finance (banks, securities, insurance, etc.), telecommunications, automotive, beverages, toiletries, and pharmaceuticals. Contributions include "Corporate Reputation" (Advertising) and "CSR and Corporate Reputation" (Nikkei Branding). Certified Member of the Securities Analysts Association of Japan.