Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

The "occasional users" segment holds the key to advancing cashless payments in Japan.

What is the current state of cashless usage in Japan?

The Dentsu Inc. Cashless Project, a Dentsu Inc. project team supporting marketing strategy in the payment domain, conducted an online "Consumer Cashless Awareness Survey" in December 2022. This survey examined how consumers utilized cashless payments in their daily lives over the preceding year. ( Survey overview here )

This survey classified cashless users into five distinct segments (types) based on the difference in their cashless versus cash usage, then tracked their usage patterns.

The results highlighted a significant gap between "heavy users" and other cashless users. This series explores insights from the survey to find clues for promoting cashless payments in Japan.

Reference Series: Cashless Japan Survey 2021: DX Driven by Cashless

<Table of Contents>

▼Classifying Consumers into Five Types Based on Usage Patterns

▼A Practical Classification Method Reveals Targets for Cashless Promotion

▼The Key Target: "Cashless-Rich Potential Users"

▼The "Cashless-RichPotential Users"Volume SegmentHas a High Proportion of Women

▼Seniors Increasing Their Presence as a "Potential User" Segment

▼Cashless-Rich Users Tend to Have Higher Incomes

▼Higher Usage Frequency Correlates with Diverse Payment Method Adoption

▼Mobile payments, not card payments, are key to advancing cashless adoption

Classifying consumers into five types based on usage patterns

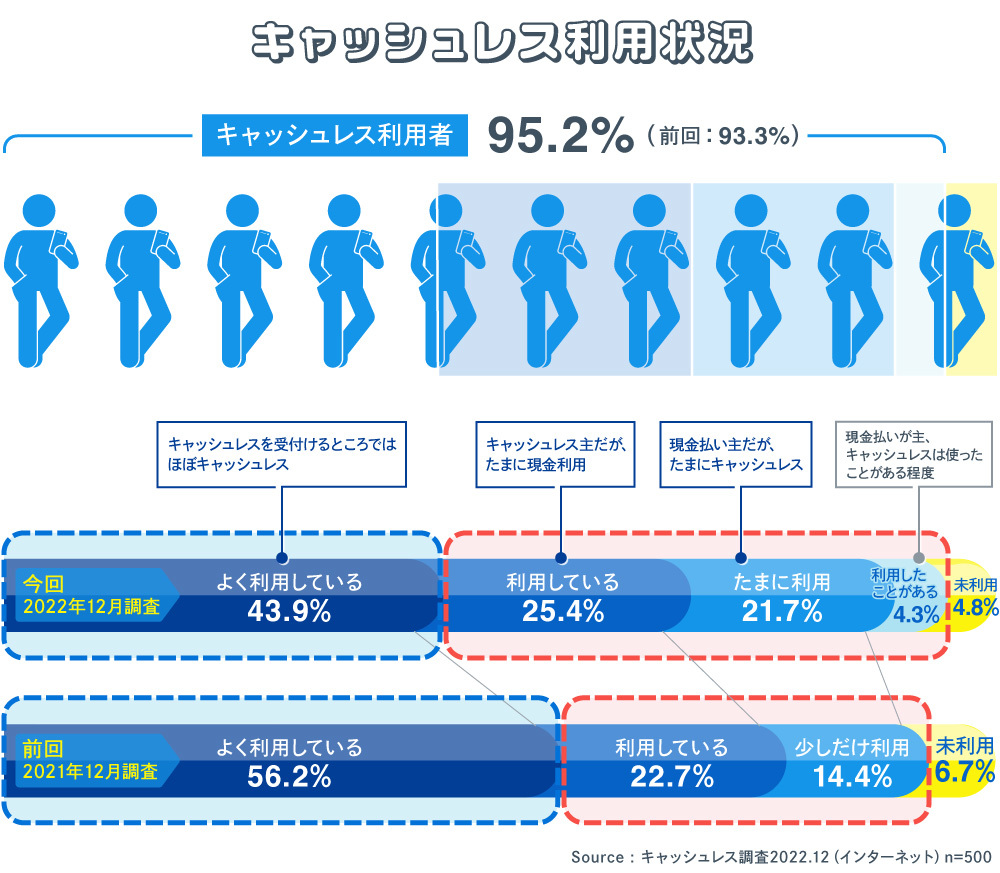

95.2% of people used cashless payments in some form over the past year. Meanwhile, 4.8% were non-users who only used cash.

In the previous survey (December 2021), cashless users were 93.3% and non-users were 6.7%. Thus, cashless users increased by 1.9%, while non-users decreased by the same amount. Based solely on this result, one might say, "In 2022, cashless users continued to increase while non-users decreased." However, while 95.2% of respondents had cashless payment experience, the actual cashless payment ratio for Japan's personal consumption expenditure in 2022 remained at only 36.0 %.

In cashless-advanced countries like South Korea and China, the cashless ratio exceeds 80% of personal consumption expenditure. So why is the spending amount in Japan not growing significantly?

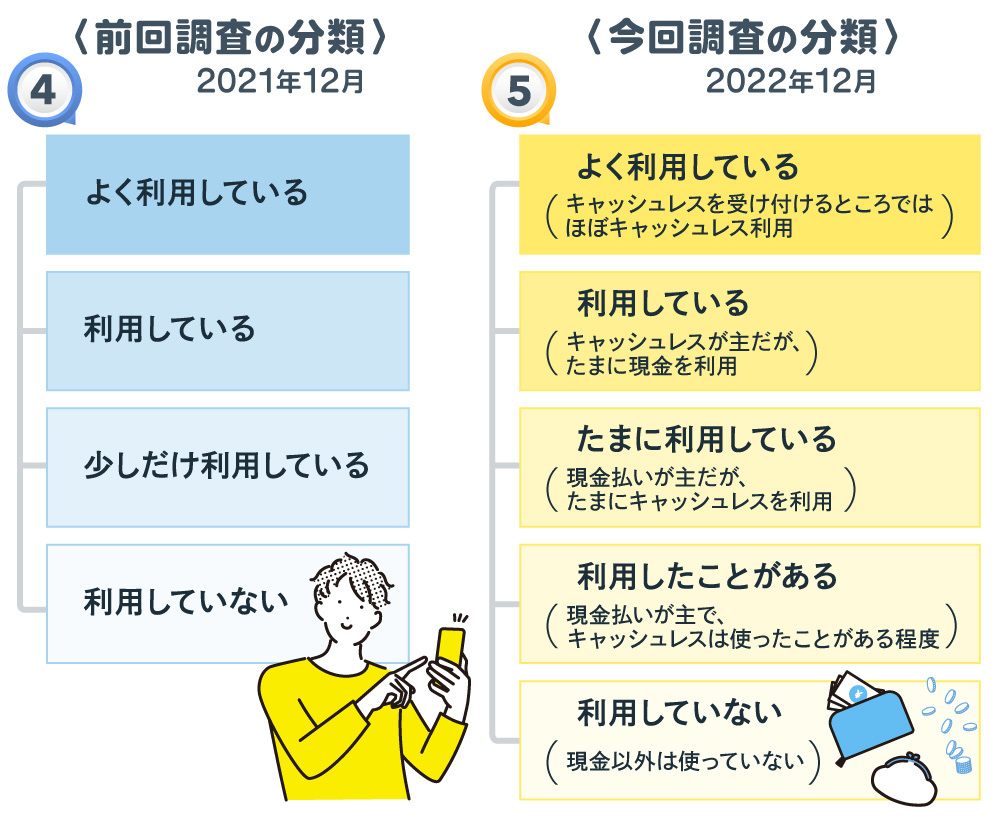

To explore this reason, this survey changed the classification of consumers from the "four types" used in past surveys to "five types" defined based on the ratio of cashless to cash usage. This allows for a clearer definition of cashless usage patterns and enables consumers to be segmented (classified by type) for detailed analysis.

A classification method aligned with reality revealed targets for cashless promotion

The results from the survey, which changed from four to five classifications, revealed different cashless usage patterns than before.

The "Frequent Users (use cashless almost everywhere that accepts it)" segment stood at 43.9%, a decrease of 12.3% from the previous survey's 56.2%.

This result can be interpreted not simply as a decrease in the number of people who "use it frequently," but rather as 12.3% of respondents choosing the next lower segment. This outcome resulted from clarifying the subjective assessment of "frequent use" by adding parentheses.

Those who "use it (cashless is primary, but occasionally use cash)" accounted for 25.4%. This represents a 2.7% increase from the previous survey's 22.7%. However, this increase is only 2.7%, not the full 12.3% shift from the "use it frequently" segment.

Those who answered "Occasionally use (primarily cash, but occasionally use cashless)" accounted for 21.7%. "Have used before (primarily cash, but have used cashless to some extent)" was 4.3%. In the previous survey, these two segments were grouped under "Use a little" (14.4%). These two items now serve as the receptacle for those who have "slipped" from the top two segments.

Compared to those who "have never used it," the people in these three segments—"using it," "using it occasionally," and "have used it"—represent a target group with potential for promoting cashless use in Japan. Looking at the graph comparing the two: it clearly shows an increase in the number of people possessing this potential ("using it occasionally" and "have used it").

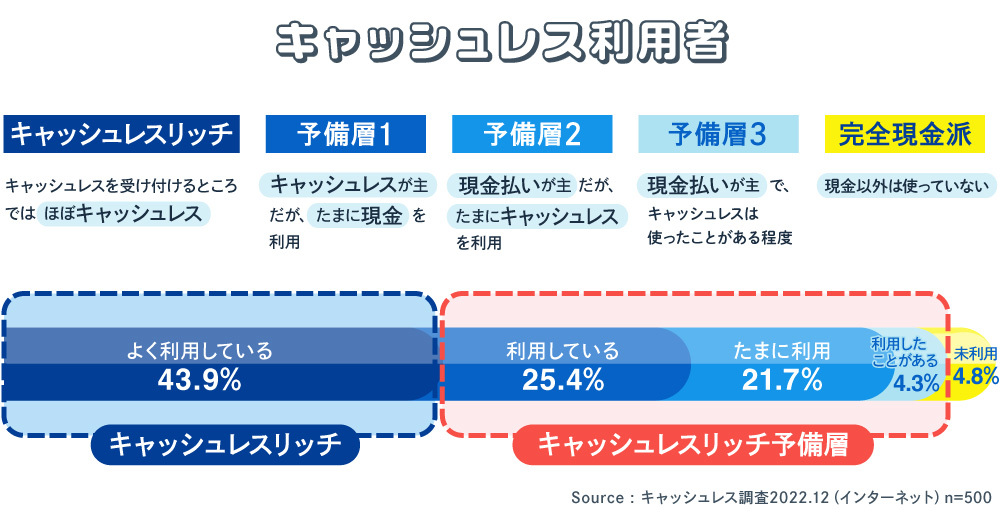

The target group to approach is the "Cashless-Rich Reserve Segment"

This time, we decided to name each of these five categories.

First, we named those who "use cashless almost everywhere that accepts it" as "Cashless Rich." They are heavy users of cashless payments.

We named "those who primarily use cashless but occasionally use cash" as "Preparatory Group 1 (Occasional Cash Users)", "those who primarily use cash but occasionally use cashless" as "Preparatory Group 2 (Occasional Cashless Users)", and "those who primarily use cash and have only tried cashless" as "Preparatory Group 3 (Cashless Beginners)".

Those who "use nothing but cash" are called "Pure Cash Users."

The three segments named "reserve groups" consist of people who primarily use cash alongside cashless payments, or those who primarily use cashless payments alongside cash. Collectively, these three segments are termed the "Cashless-Rich Reserve Groups."

The Cashless-Rich Reserve Segment accounts for 51.4% of the market, surpassing the Cashless-Rich Segment (43.9%) in scale. Among them, Reserve Segment 1 and Reserve Segment 2 comprise the largest numbers of users.

We believe that once someone has used cashless payments even once, it shouldn't be difficult to increase their frequency or amount of cashless transactions in some way. In other words, promoting cashless usage among this volume zone population will undoubtedly accelerate Japan's cashless adoption rate.

The "Cashless Rich Potential Users" segment within the volume zone has a higher proportion of women.

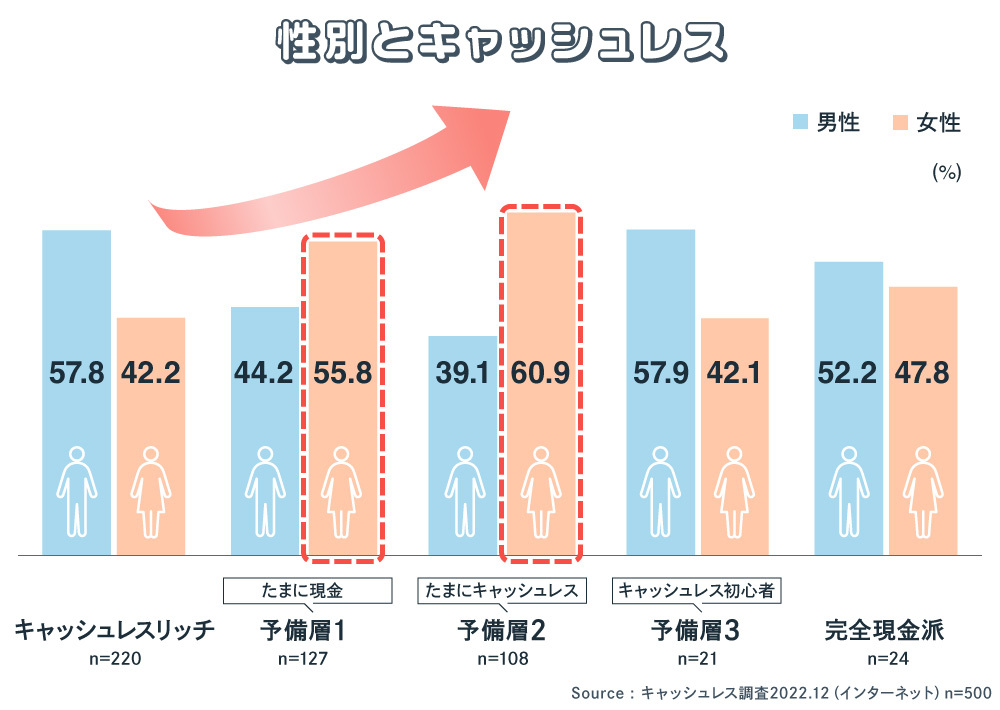

Next, we'll highlight the characteristics of the five segments. First, let's look at gender. In this survey, the gender distribution is evenly split between men and women.

The "Cashless Rich" segment is the largest group, comprising 220 of the 500 total respondents. These are people who use cashless payments almost exclusively wherever they are accepted. The gender composition within this group was 57.8% male and 42.2% female, showing a male majority.

The next largest group is "Reserve Group 1 (Occasional Cash Users)" with 127 people. They primarily use cashless payments but occasionally use cash. The gender breakdown shows 55.8% female and 44.2% male, indicating a female-dominated group. "Reserve Group 2 (Occasional Cashless)" is the third largest group with 108 members. These individuals primarily pay with cash but occasionally use cashless methods. The gender breakdown shows 60.9% female and 39.1% male, with a particularly high proportion of women.

"Reserve Group 3 (Cashless Beginners)" is a minority group of 21 people. They primarily pay with cash and have only tried cashless payments to some extent. Men accounted for 57.9%, women 42.1%. The "Pure Cash Group" is a minority group of 24 people. They use nothing but cash. The gender breakdown was 52.2% male, 47.8% female.

The graph shows that for men, the percentage declines steadily from Cashless Rich to Reserve Group 1 and Reserve Group 2. For women, the opposite is true—the percentage increases steadily. This result suggests the potential for increased cashless usage among women.

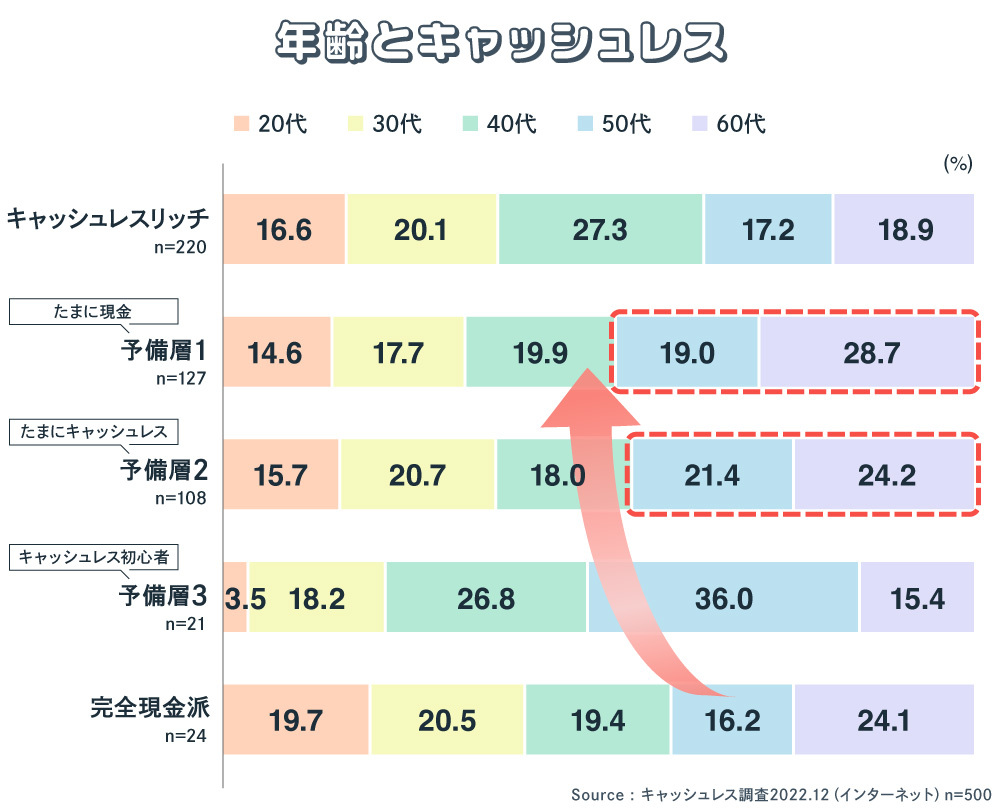

The Growing Presence of Seniors as a "Reserve Group"

What relationship exists between age and cashless usage? The survey ensured age groups were evenly distributed.

Looking at the age composition of "Cashless Rich" users, those in their 40s were the most numerous (27.3%). This was followed by those in their 30s (20.1%), 60s (18.9%), 50s (17.2%), and 20s (16.6%). This was an unexpected result, as it was initially assumed that younger age groups would have higher cashless usage.

Conversely, the largest group in "Reserve Group 1 (Occasional Cash Users)" was those in their 60s (28.7%). This was followed by those in their 40s (19.9%), 50s (19.0%), 30s (17.7%), and 20s (14.6%). Similarly, for "Preparatory Group 2 (Occasionally Cashless)", the largest group was those in their 60s (24.2%). This was followed by those in their 50s (21.4%), 30s (20.7%), 40s (18.0%), and 20s (15.7%).

For "Preparatory Group 3 (Cashless Beginners)", the largest group was those in their 50s (36.0%). This was followed by those in their 40s (26.8%), 30s (18.2%), 60s (15.4%), and 20s (3.5%). Finally, for "Pure Cash Users", the largest group was those in their 60s (24.1%).

As the graph clearly shows, the 50s and 60s age groups are a significant and unignorable segment among the Cashless Rich Potential Group. Therefore, encouraging higher age groups to use cashless payments more, rather than focusing solely on the younger 20s demographic, is arguably the key to promoting cashless adoption.

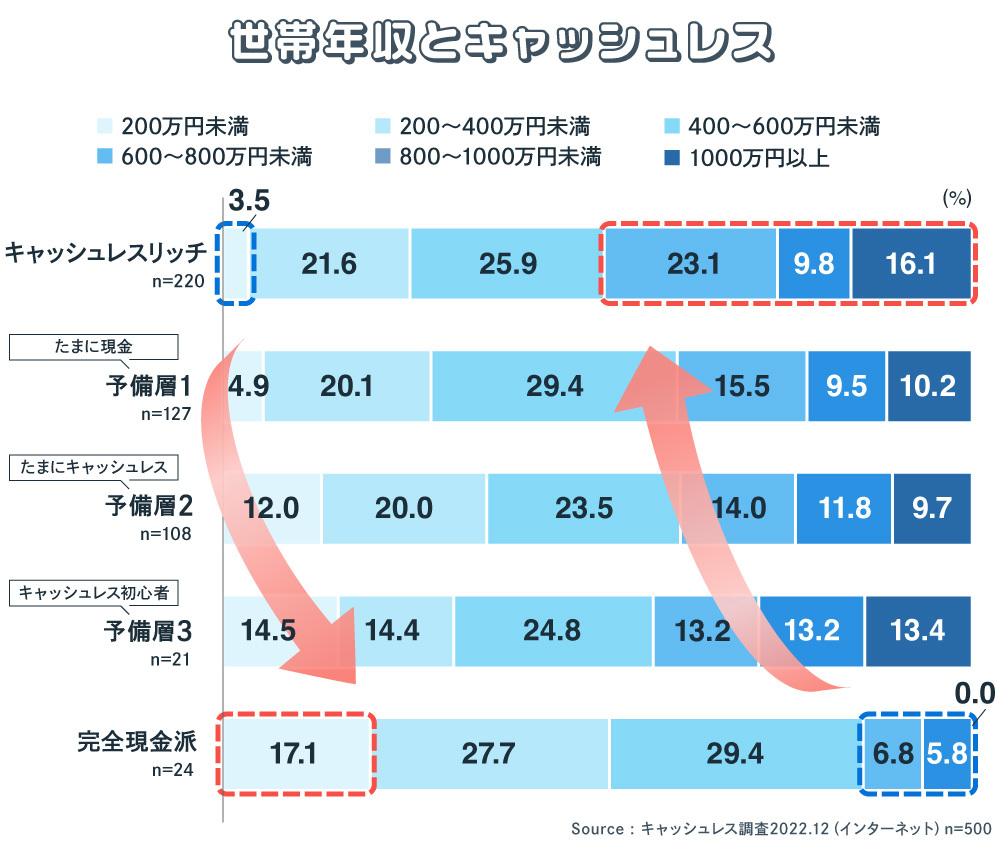

Cashless Rich tend to have higher incomes

What is the relationship between annual income and cashless usage? We calculated the ratio using only those survey respondents who declared their annual income (excluding those who answered "don't know" or left it blank).

Looking at income segments, among those earning less than ¥2 million annually, "Strict Cash Users" were the largest group (17.1%), "Preparatory Group 3 (Cashless Beginners)" at 14.5%, "Preparatory Group 2 (Occasional Cashless Users)" at 12.0%, "Preparatory Group 1 (Occasional Cash Users)" at 4.9%, and "Cashless Rich" at 3.5%. This shows a clear trend: the higher the income, the fewer the Cashless Rich.

In contrast, among those with an annual income of ¥10 million or more, "Exclusively Cash Users" accounted for 0%. While "Preparatory Group 3 (Cashless Beginners)" accounted for 13.4%, "Preparatory Group 2 (Occasional Cashless Users)" was 9.7%, "Preparatory Group 1 (Occasional Cash Users)" was 10.2%, and "Cashless Rich" was 16.1%. This shows a trend where the more cashless usage increases, the larger the group becomes. Cashless Rich individuals might also be considered wealthy in terms of annual income.

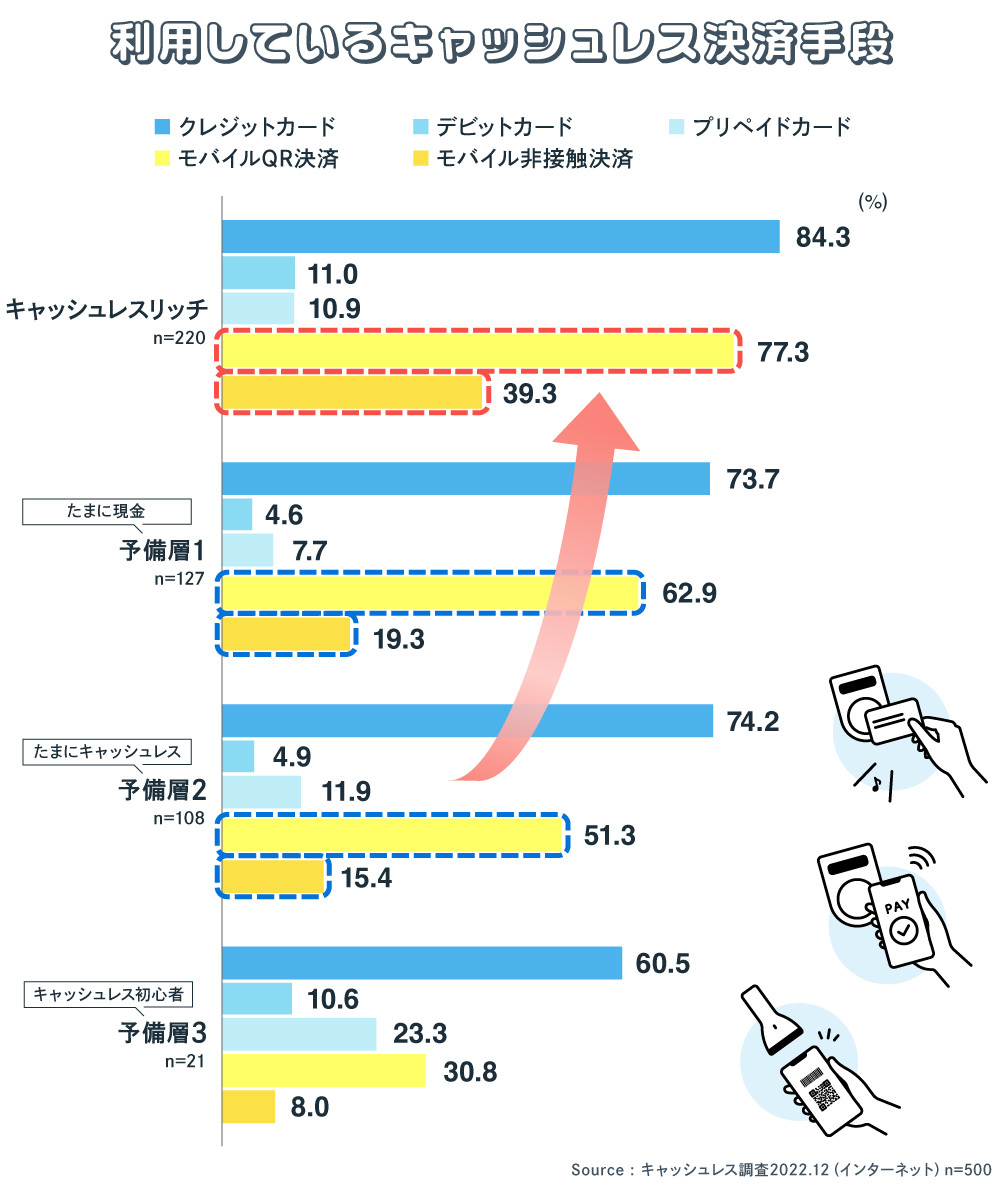

Higher Usage Frequency Correlates with More Diverse Payment Methods

What payment methods do cashless users employ? Credit cards were the most common (78.1%). However, this represents a 3.8% decrease from the previous year (81.9%). The second most frequently used method was mobile QR payments (65.5%), showing a 1.8% increase from the previous year (63.7%).

These results clearly show that credit cards and mobile QR payments are the two primary payment methods for cashless users. So, what happens when we break down payment methods between "Cashless Rich" and the "Reserve Group"?

The "Cashless Rich" group uses a wider variety of payment methods than the Reserve Group. Credit cards were used by 84.3%, mobile QR payments by 77.3%, and mobile contactless payments by 39.3% – all higher than the Reserve Group.

The "Reserve Group 1 (Occasionally Cash)" segment resembles a scaled-down version of the Cashless Rich, while the "Reserve Group 2 (Occasionally Cashless)" segment shows a tendency to be a scaled-down version of Reserve Group 1. Within this landscape, mobile QR payments and mobile contactless payments demonstrate high potential and significant room for growth.

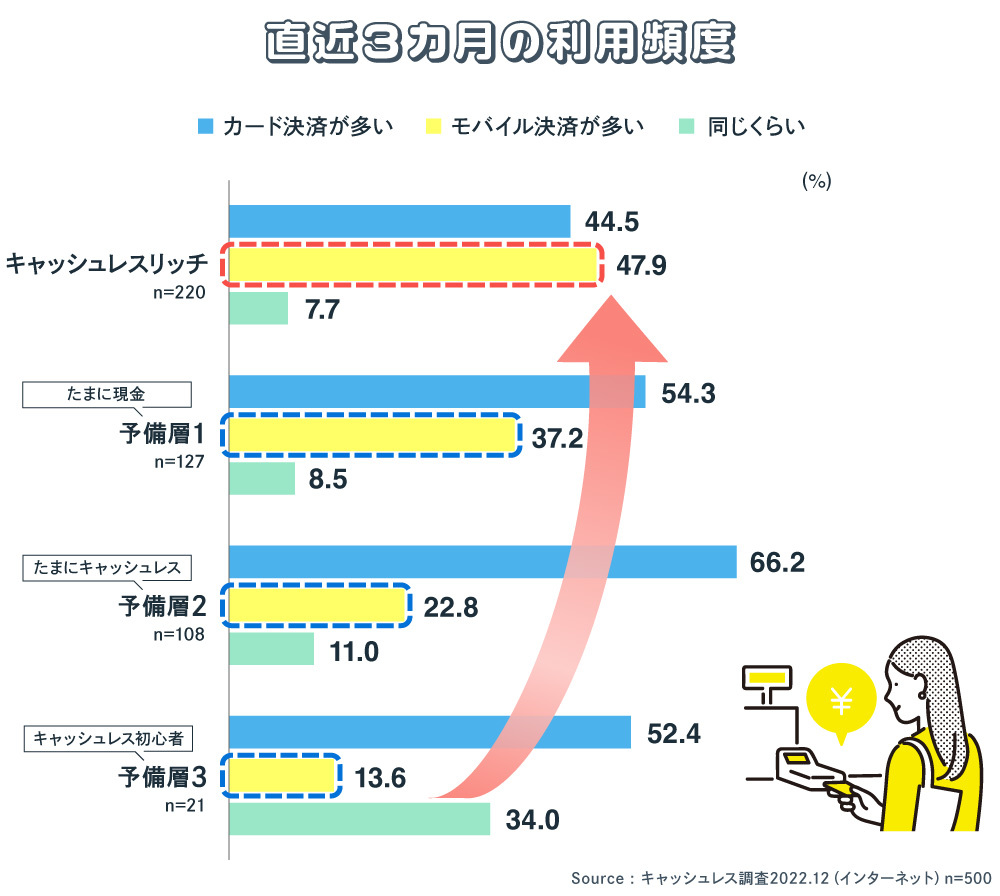

Mobile payments, not card payments, are the key to advancing cashless adoption

We further asked respondents to limit their cashless payment methods to the past three months and specify whether they used "card payments more" or "mobile payments more." This revealed a different aspect compared to the previous results.

Among "Cashless Rich" users, mobile payments (47.9%) were more common than card payments (44.5%). This indicates that people who use cashless payments almost exclusively where accepted have a high frequency of mobile payment use in their daily lives.

This likely stems from their conscious focus on cashless payments during regular shopping. Many shops handling small transactions tend to accept only mobile payments. The profile of "Cashless Rich" consumers emerges: even if cards aren't accepted, they use mobile payments where available.

Among those who frequently use card payments, 54.3% fall into "Reserve Group 1 (occasional cash users)", while this increases to 66.2% in "Reserve Group 2 (occasional cashless users)". Conversely, among those who reported frequent mobile payment use, the proportions decrease in the order of Reserve Group 1, Reserve Group 2, and Reserve Group 3. In daily life, while people might forget their wallet or cards, they rarely forget their smartphone. If mobile payment usage—often accepted even at small-ticket shops—can be further promoted, cashless usage may increase even more.

Next time, we will examine cashless usage and point usage in Japan to uncover hints for promoting cashless payments going forward.

[Survey Overview]

Title: "Cashless Awareness Survey of Consumers"

Survey Method: Online survey

Survey Period: December 12-15, 2022

Survey Area: Nationwide

Survey Participants: 500 men and women aged 20–69 (weighted based on population composition)

Survey Sponsor: Dentsu Inc., Dentsu Cashless Project

Research Company: Dentsu Macromill Insight, Inc.

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Author

Yoshitomi Sairyo

Dentsu Inc.

BX Creative Center, Experience Design Department

Senior Planning Director

Head of the Dentsu Cashless Project. Joined Dentsu Inc. after working at a U.S.-based consulting firm and a European investment bank. Engaged in new business development, marketing and brand strategy, and PR for clients in finance (banks, securities, insurance, etc.), telecommunications, automotive, beverages, toiletries, and pharmaceuticals. Contributions include "Corporate Reputation" (Advertising) and "CSR and Corporate Reputation" (Nikkei Branding). Certified Member of the Securities Analysts Association of Japan.