Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

The New Relationship Between Money and Emotion: The Future of Money as Envisioned by FinTech Startups.

Shinichi Takatori

Kyash Inc.

Tomoya Okuya

Dentsu Inc.

A series of interviews spotlighting venture companies transforming societal norms through innovative breakthroughs, exploring their business philosophies and envisioned futures. This installment features Kyash, a venture company attracting significant attention in the FinTech domain by merging finance and technology. The company developed a new remittance system via smartphone app. Its CEO, Shinichi Takatori, conversed with Tomoya Okutani, who promotes hands-on support for venture companies at Dentsu Inc.

To people, to stores. Could money transfers and payments be realized together? The financial app born from that idea

Okutani:Kyash was founded in 2015 and is creating a new remittance platform in the FinTech space. First, could you tell us what kind of business you are running?

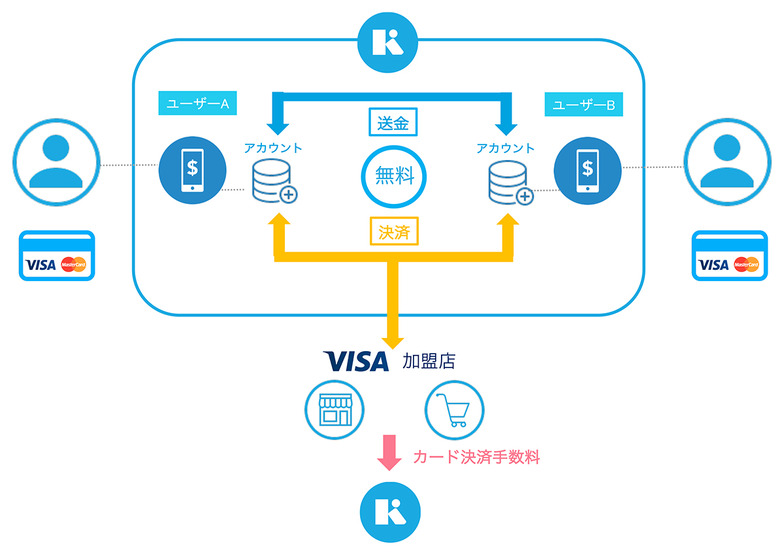

Takatori: It's a money transfer service via smartphone app. By linking a credit card to the app, users can easily send money or make payments directly from their phone. A key feature is that while "payment" typically means sending money to a store, this app also enables sending money to individuals.

Okutani: Being able to send money to individuals using the same app as for store payments is innovative, right? When positioning players in the FinTech space, "money transfers" and "payments" are often categorized separately. Kyash, however, handles both within a single platform.

Takatori: Exactly. In today's world where e-commerce is commonplace, online payments to stores are routine. But when it comes to peer-to-peer transactions, they've always been handled through completely different channels. I've recognized this as an issue since my days as a banker. I thought that by designing things more from the user's perspective, we could actually merge payments to stores and individuals onto the same platform. We're now ready to offer this through our own legally compliant system.

Okutani: What kind of service will this actually be?

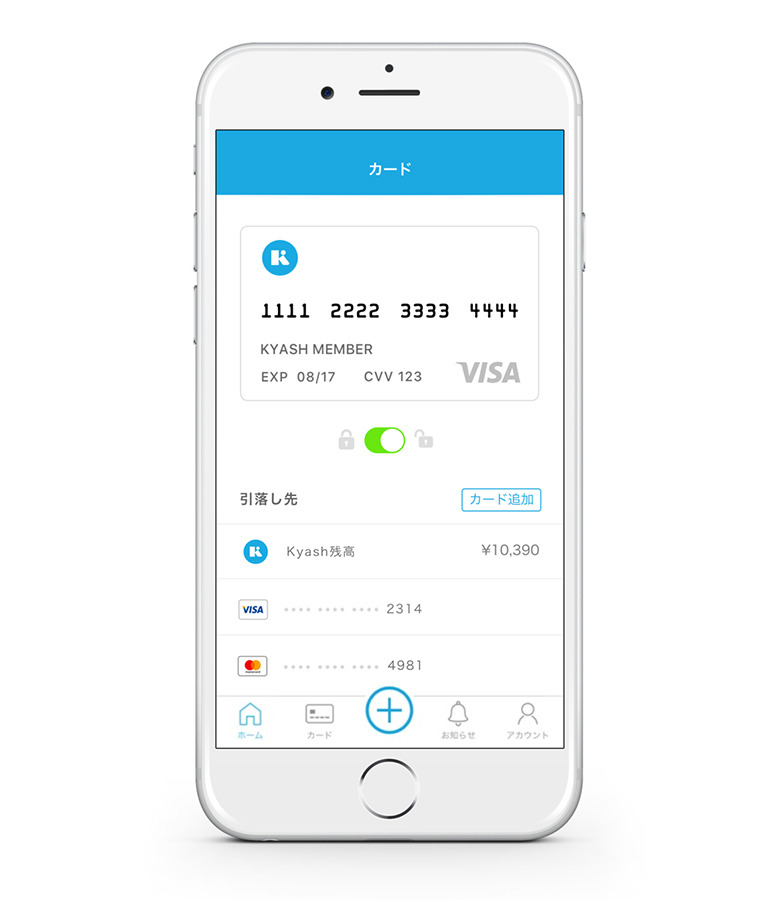

Takatori: When you download the app, you get an account linked to a dedicated Visa card. You then connect your existing personal credit cards to this account. Using this as a base, you can send money to friends connected via social networks, phone numbers, or email addresses, starting from as little as one yen. You can also send, say, 500 yen with a message like "Paying you back for yesterday's coffee!" or attach a photo.

There's also a "Request" feature. When you request money from someone, they receive a notification. If your friend

If they approve, the money is sent to the requester. They can also decline.

The received balance can be used directly at stores like a regular credit card by using the 16-digit number on the Visa card issued through the app.

When the hassles of consumption disappear, your lifestyle becomes richer

Okutani: It seems like it could also solve the hassle of money transactions.

Takatori: I believe it will streamline group spending, which has always felt cumbersome. For example, splitting the bill at a drinking party or paying for a taxi shared by four people often can't be handled on the spot and becomes a hassle. It's especially difficult when you don't know when you'll next meet those people. This might be one factor holding back group spending. If we can solve this with "Kyash," group activities could become simpler and more active. We actually want to be the solution that smooths out the money exchanges people find stressful.

Okutani: I think Japanese people, in particular, have a psychological tendency to avoid money issues. It might even be hard to ask someone you see regularly to "pay me back." By eliminating that stress while retaining the communication element within the app, money exchanges become less inconvenient, broadening the scope of spending behavior.

Takatori: We're already seeing more people split bills using e-commerce gift cards. I believe our solution could gain acceptance as an even more versatile method.

Okutani: So the demand is already apparent.

Takatori: Also, this is a bit further down the road, but I believe it connects to the culture of tipping and donations. My parents used to host international students, so I was constantly asked, "Why don't Japanese people tip?" This exposed me to the idea of systems that make it easy to exchange value.

Okutani: So you mean it functions as an incentive?

Takatori: Exactly. If tipping culture catches on, staff providing good service would receive incentives, boosting their motivation. For customers, if tipping becomes widespread, the service charge would be deducted from the actual listed price, potentially lowering the surface price. This would ensure money reaches those who deserve it and allow value to be transferred based on genuine sentiment. I believe it could create a new economic cycle for society.

Our business operates in finance and IT, but it's crucial that we go beyond that to enrich the lives and lifestyles of our users. We want to create a product that makes that possible.

Okutani: Business must generate economic value, of course, but I also believe it cannot grow without social value. Even if it grows, alternatives may emerge or new players enter the market. But with social value, customers resonate with the greater purpose, so we strongly emphasize that aspect.

The Future Financial Services I Should Create, Coming from a Banking Background

Okutani: Next, I'd like to hear about your background and the journey to founding Kyash. What was your career path before launching Kyash?

Takatori: I worked at a bank for five years, then spent just under two years as a strategy consultant in the consumer sector. Starting in my third year at the bank, I handled overseas operations. Since banking models and laws differ by region, it was a valuable learning experience for understanding infrastructure elements. For example, banks in North America can issue credit cards, and in South America, they can even handle securities operations. The industry structure is completely different from Japan, where banks, securities firms, and card companies are separate entities.

Okutani: So seeing these international differences made you aware of the challenges in Japan's financial legal framework and structure?

Takatori: Yes, that's right. Furthermore, during my consulting days, I witnessed firsthand how the proliferation of smartphones amplified individual influence. Observing how consumers make decisions, I realized that the financial industry would also need channels much closer to the user going forward.

Okutani: So, first you learned about the diversity of industry structures during your banking days, and then during your consulting days, mobile emerged as something that drastically changed consumer behavior. Your current business model was born from challenges identified in both areas.

Takatori: Looking 10 or 20 years ahead, it was clear that smartphone adoption and digitalization would advance. That meant laying the groundwork for this shift in finance too. However, banks face a dilemma: their long-held public trust and fairness obligations make it difficult to make partially optimal decisions. Therefore, I decided to start Kyash with a sense of mission – to pioneer as an industry-savvy operator and later collaborate with financial institutions.

Okutani: Indeed, we've seen financial institutions increasingly partner with startups to leverage new technologies, and we often support such open innovation initiatives. By the way, did you aim to develop a mobile-centric money transfer service from the very beginning?

Takatori: Yes, we did. So, first and foremost, we conducted extensive research. Since there was a university near our home, we even approached college students directly to conduct surveys (laughs). Beyond that, we pored over banking-related literature and research reports.

Okutani: It's common for companies to pivot when a product they believe is good fails to resonate with the market. Understanding market viability is crucial—like conducting surveys with actual university students to get raw feedback—and it's something we also prioritize.

If you can transfer "value" based on genuine emotion, it creates a proper value cycle.

Takatori: After founding the company, we first launched a system that allows credit cards to be used with a sense of security similar to carrying cash in a wallet. Driven by our desire to contribute to safe and secure card usage, we released a system for financial institutions that provides real-time notifications of card usage.

Even then, we envisioned building remittance and payment systems in the medium to long term. However, we recognized that such systems carry the risk of user losses, requiring substantial trust and expertise to launch. Therefore, in the first phase, we developed products that contribute to a safe and secure user environment. We've built our remittance system foundation on the robust system architecture cultivated through this work.

Okutani: What do you think will be key for the widespread adoption of these remittance apps in the future?

Takatori: Money transfers and payments are means of exchanging value. For adoption in this space, the product must first be easy for users to adopt. It must also be usable anywhere—meaning it has liquidity. It will only be used where these two axes intersect.

Okutani: Regarding user-friendliness, UI/UX is crucial. Younger users especially prioritize that sense of experience, and your app clearly demonstrates thoughtful design in this area.

Takatori: Thank you. Regarding the other aspect of liquidity, while e-money usable at specific sites or stores and points dependent on card companies are widespread now, they often have limited usage scope, right? Creating a system where value can be used more cross-platformly—that's what we aim for.

Okutani: True. Precisely because points have limited uses, no service has yet established an overwhelming position in the remittance or payment space.

On the other hand, if this app catches on, I think it could first be applied to splitting bills. But beyond that, there seems to be another step up. As this system becomes more widespread, it might even be usable for donations or crowdfunding.

Takatori: That's a crucial point. Our goal is to "create a proper value cycle." I felt a sense of mission during the Kumamoto earthquake too. Immediately after the disaster, many donation channels were set up, but most required bank transfers. Even if 100 people wanted to donate, few

not many people are in a position to make a bank transfer immediately. If we could make this much easier, anytime and anywhere, the amount of money moving would change, and the impact it creates would change too.

Okutani: Simply simplifying the donation method can drastically change the outcome. If technology can handle that, donations could become commonplace, creating immense social value.

Takatori: When sending money and payments become easy, we can transfer the value of "money" based purely on emotion and feeling. That way, value should reach the intended recipient directly. Our company wants to keep pursuing this future of currency alongside our products.

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Author

Shinichi Takatori

Kyash Inc.

Chief Executive Officer

After graduating from Waseda University, he joined Sumitomo Mitsui Banking Corporation. Following corporate sales, he worked as a corporate planning officer responsible for establishing overseas bases, partnership strategies with financial institutions, new business ventures, and overseas investment projects. He then worked on new B2C ventures at the Japan and US offices of a US-based strategic consulting firm. Founded Kyash in January 2015 and launched the completely free money transfer app "Kyash" in April 2017. Served as a director of the FinTech Association (General Incorporated Association) since September 2015.

Tomoya Okuya

Dentsu Inc.

Director of Integrated Marketing Production

After working in marketing, sales, creative, digital, and business development departments, he assumed his current position. He is engaged in supporting clients' marketing efforts, as well as business development and investment in the technology sector, and promoting open innovation. His experience as a lecturer and judge includes "AdTech Tokyo," "The FinTech Center of Tokyo FINOLAB Inc./MEET UP with FINOVATORS," "Incubation & Innovation Initiative/Mirai," "Japan Startup Association," and others.