Note: This website was automatically translated, so some terms or nuances may not be completely accurate.

Media Trends Seen in the Development of UK Television Broadcasting Services

With the advent of digitalization and the evolution of internet technology, television broadcasting has begun offering a variety of services that transcend traditional boundaries. Here, we will consider the direction of television media development by introducing the evolution of television broadcasting services in the UK, which pioneered the digitalization of terrestrial broadcasting ahead of other nations.

Why focus on the UK case?

The UK's broadcasting market structure, where the public broadcaster BBC coexists with commercial broadcasters, is quite similar to Japan's. The BBC, primarily funded by license fees (equivalent to Japan's reception fees), is expected to provide highly public-interest programming and pursue advanced initiatives. This BBC, along with the three major commercial broadcasters led by ITV, forms the core of the UK's broadcasting market.

These traditional broadcasters have implemented various strategies to reach a wider audience. This contrasts with the US, where entry from other industries and tech-backed startups often disrupts existing broadcasting models. From these perspectives, the UK represents a reference market for Japan when considering the future of broadcasting services.

The appeal of digital broadcasting in the UK is "multiple channels."

Unlike the US and many European countries where paying to watch TV is common, the UK is characterized by the significant presence of free terrestrial broadcasting as a counterpoint to satellite and cable services, which are primarily pay-TV.

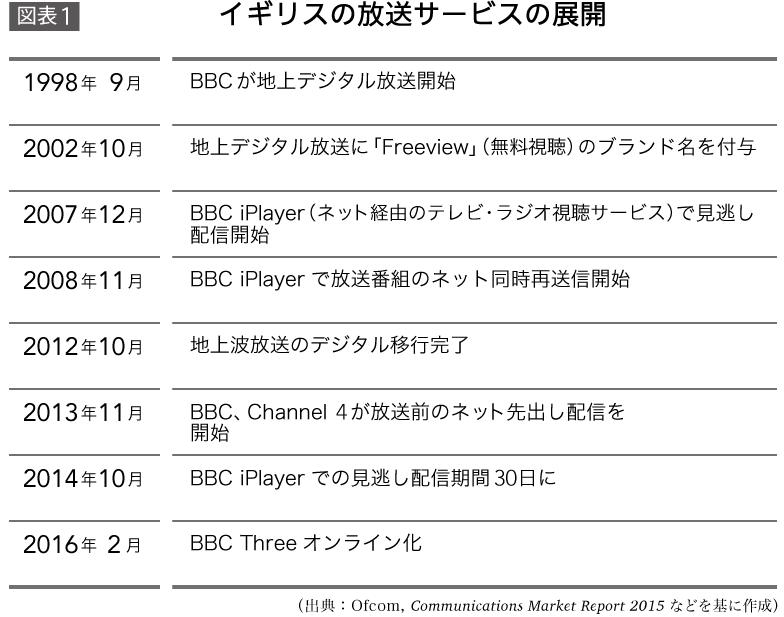

Digital terrestrial broadcasting began in the UK in 1998. A major difference from Japan, where terrestrial broadcasting achieved higher picture quality through digitization, is that the UK focused on expanding the number of channels. In the UK, which originally had few channels, multi-channel broadcasting was seen as the most obvious benefit of digitization. However, the initial business model, which leaned towards a pay-TV approach, was not accepted by consumers, leading to chaos including the bankruptcy of operating companies.

Consequently, in 2002, the industry branded terrestrial digital broadcasting as "Freeview" to boost its adoption. To put it bluntly, just as "Jidigi" (a colloquial term for terrestrial digital broadcasting) is widely used in Japan, in the UK, the name "Freeview" – which simply signifies "free-to-view" broadcasting – came to represent terrestrial digital broadcasting itself.

The core operation of Freeview is managed by major broadcasters including the BBC and ITV. Currently, viewers can access 60 SD (standard definition) channels plus 15 HD (high definition) channels. Furthermore, by connecting compatible TVs or tuners to the internet, users can utilize the catch-up streaming services provided by broadcasters, as described later. Through this environment, television sets have come to play a significant role in the UK as a device for accessing free online streaming services, alongside computers and smartphones.

Time Shift Channel: A Strategy for Expanding Reach

Leveraging the multi-channel environment, many commercial broadcasters launched "Time Shift Channels" in the 2000s. These channels broadcast programs and commercials exactly as they aired, one hour behind the original schedule.For example, ITV offers its time-shift channel, ITV+1, across various broadcast platforms including terrestrial and satellite. This time-shift channel is an extremely convenient service for viewers who do not own a DVR or lack broadband access, preventing them from using catch-up streaming services.

So, how widely are timeshift channels actually used?

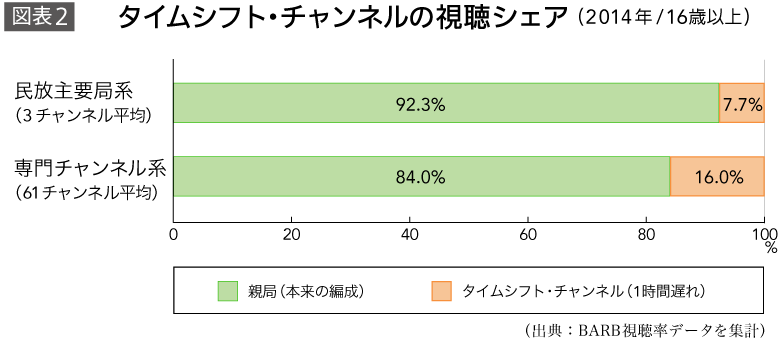

Let's examine the viewership share of the timeshift channel, calculated as a percentage of the combined total (parent channel + timeshift channel) set at 100%, based on full-year 2014 TV ratings data (for viewers aged 16 and over) [Figure 2]. For the three major commercial broadcasters (ITV, Channel 4, Channel 5), timeshift channel viewing accounted for 7.7% of the total.

*Channel 4 is a public broadcaster but operates on commercial advertising revenue, so it is included among commercial broadcasters in this article.

Meanwhile, among the 61 specialty channels (such as children's and documentary channels) that operate timeshift channels, this share reaches 16.0%. This suggests that when desired programs overlap, channels catering to specific interests and preferences are more likely to be watched at different times.

From the broadcaster's perspective, timeshift channels increase viewing opportunities and expand program reach. In fact, for advertising transactions, timeshift channel viewership is combined with the main channel's viewership and is not traded separately.

While the increasing use of online program distribution may eventually render timeshift channels obsolete, the move by broadcasters to utilize existing transmission paths to provide timeshift viewing opportunities themselves is highly unique. This stems from the creation of a multi-channel environment through broadcast digitization, and the fact that in the UK, viewing via recorded playback using devices like VCRs has been included in ratings measurement for up to seven days after broadcast since 1991.

Toward Further Expansion of "Television" ~ Anytime, Anywhere, on Any Device

In response to the spread of the internet, UK broadcasters are actively streaming their programs online. The BBC pioneered this with the launch of its catch-up service, "iPlayer," in December 2007. Initially available only on PCs, the range of compatible devices has since expanded significantly. Today, iPlayer can be accessed on PCs, tablets, smartphones, and TV sets.According to January 2016 monthly usage statistics (based on access counts), device usage breakdown was: Mobile (including tablets) 41%, TV sets 29%, PCs 26%. This shows no concentration of usage on any specific device (Source: BBC, iPlayer Monthly Performance Pack, January 2016 ).

Commercial broadcasters have also successively launched similar catch-up services. Initially, a 7-day window after broadcast was standard, but in recent years, extending the availability period to within 30 days after broadcast has become increasingly common. Furthermore, beyond catch-up services, simultaneous retransmission of programs with cleared rights is also being implemented.

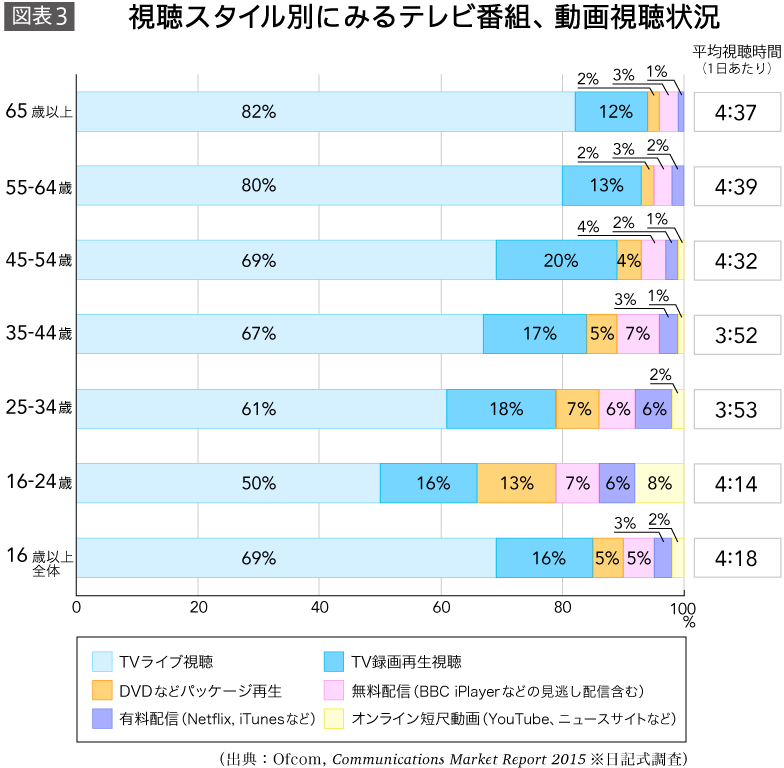

As a result, television viewing styles, which were previously limited to live viewing or recorded playback, have diversified. Among younger audiences, in particular, the tendency to watch television programs according to their own convenience has become stronger [Figure 3].

BBC Three Ceases Broadcasts to Become an "Online-Only Channel"

While the UK sees active online utilization by broadcasters, the BBC's announcement that its youth-targeted BBC Three channel would cease terrestrial broadcasts and offer content exclusively online caused surprise.

Launched in 2003, BBC Three was regarded as a "cutting-edge" channel that aired experimental programming. Consequently, the move drew significant criticism, with many questioning whether it amounted to "abandoning those without online viewing capabilities." However, while taking measures such as airing some programs on the flagship channel BBC One, BBC Three ceased terrestrial broadcasting in February 2016 and transitioned online under the same brand name.The BBC stated it would focus on developing new program formats tailored for the internet.

The decision to cease broadcasting on an existing channel and move entirely online is likely unprecedented globally. The BBC cites financial constraints and the need to engage younger audiences as reasons for this move.The shift of young audiences to online platforms is a challenge for the UK broadcasting industry. By providing content online, the BBC aims to maintain its brand and reach. While no other broadcasters appear to be following this lead, it stands as a recent example of a broadcaster itself expanding the definition of "television," making its future developments worth watching.

Cross-platform measurement: A challenge for the UK broadcasting industry

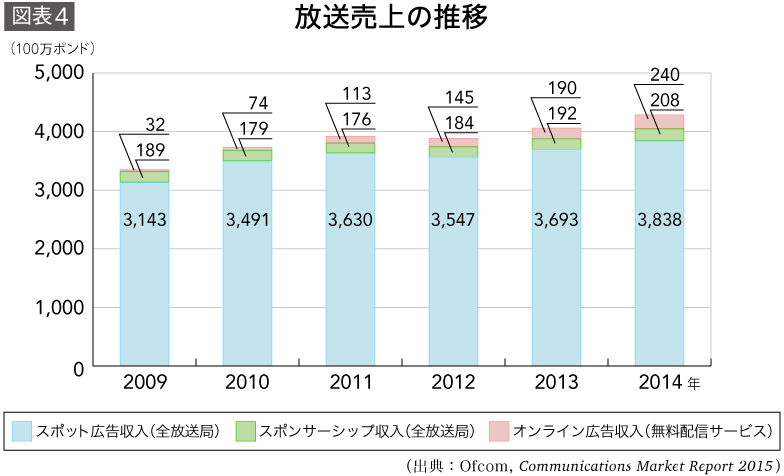

While the UK broadcasting industry is advancing content delivery unconstrained by device, transmission path, or distribution format, the challenge lies in visualizing viewing trends. For commercial broadcasters, particularly those reliant on advertising revenue, accurately grasping and monetizing online viewing is crucial for sustainable service operation.For commercial broadcasters, ads on catch-up services are sold separately (see online advertising revenue in [Figure 4]), but this revenue remains relatively small compared to advertising income from traditional broadcasts. However, advertising revenue from online distribution is a growing area, making cross-platform audience measurement across devices and platforms a major challenge.

The British Audience Research Broadcasters (BARB), the UK's audience measurement and management organization, has been implementing measures such as installing measurement apps on the viewing devices of panel households. It has been gradually publishing the results of these efforts since 2015.

Considering the Future of Japanese Broadcast Services from UK Initiatives

Advancements in technology and infrastructure are dramatically expanding the ways people access information and entertainment.The emergence of new technologies and services will likely continue to transform consumers' media environments, making it difficult to predict the exact direction of these changes. While not all initiatives by UK broadcasters will succeed, there are significant lessons to be learned from their approach to adapting to the changing consumer environment, their efforts to increase program viewing opportunities across devices and transmission channels, and the cross-industry movement towards realizing cross-platform measurement.

Was this article helpful?

Share this article

Newsletter registration is here

We select and publish important news every day

For inquiries about this article

Back Numbers

Author

Mariko Morishita

Dentsu Inc.

Marketing Administration Center, Media Innovation Research Department (Dentsu Inc. Media Innovation Lab)

After working in the theater industry and research institutions, he joined Dentsu Inc. He conducts extensive research and studies on the impact of technological innovation on the information media market, focusing on audience trends. He also monitors developments in the broadcasting industry and related policies in Western countries.

dentsu Media Innovation Lab

Dentsu Inc.

Launched in October 2017, leveraging Dentsu Inc.'s longstanding media and audience research expertise. Conducts research and disseminates insights to capture shifts in people's diverse information behaviors and understand the broader media landscape. Provides proposals and consulting on the communication approaches companies need within this context.